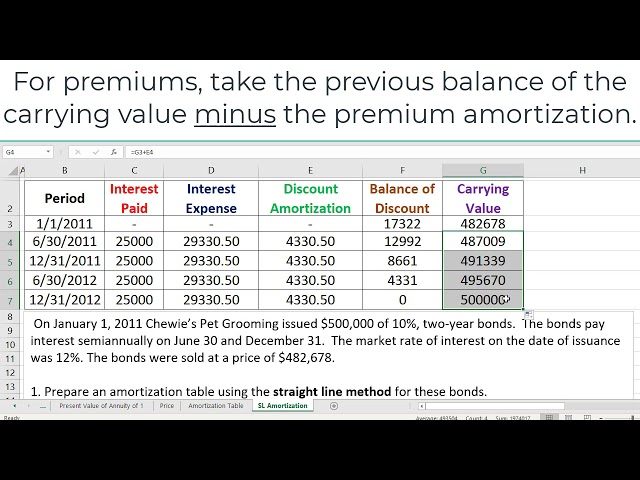

Straight line discount amortization defines a method for allocating a discount on a loan or investment over its lifetime. For instance, if a company issues a bond with a face value of $1,000 and sells it for $950, the $50 discount is amortized over the life of the bond, reducing the carrying value on the company’s balance sheet.

Straight line discount amortization is commonly used because of its simplicity, providing a consistent reduction in carrying value. The concept has been used for centuries, with a significant development in the 19th century when accountants began applying it to bond valuation.

This article will delve into the mechanics of calculating straight line discount amortization, outlining the steps and formulas involved. Furthermore, it will explore advanced applications and considerations for this amortization method within accounting frameworks.

How to Calculate Straight Line Discount Amortization

Discount amortization is a crucial accounting method for spreading the discount on a loan or investment over its lifetime. Key aspects of this calculation include:

- Face Value

- Sale Price

- Discount

- Amortization Period

- Amortization Rate

- Carrying Value

- Interest Expense

- Effective Interest Rate

- Present Value

These aspects collectively impact the calculation and recording of discount amortization. For example, the amortization period determines the number of periods over which the discount is spread, while the amortization rate establishes the portion of the discount amortized in each period. By understanding these key aspects, accountants can accurately apply the straight line discount amortization method.

Face Value

Within the context of calculating straight line discount amortization, “Face Value” holds significant importance as the principal amount of a loan or investment. It serves as the benchmark against which the discount is calculated and amortized over the loan or investment’s lifetime. A clear understanding of Face Value is crucial for accurate amortization calculations.

When a loan or investment is issued at a discount, its Face Value exceeds the Sale Price. The discount, which represents the difference between the Face Value and the Sale Price, is amortized over the life of the loan or investment, resulting in a gradual reduction of the carrying value on the issuer’s balance sheet. Straight line discount amortization allocates the discount evenly over the amortization period, providing a consistent reduction in carrying value.

In practice, Face Value plays a critical role in various financial transactions. For instance, in bond issuance, the Face Value determines the amount that the bondholder will receive at maturity. Similarly, in loan agreements, the Face Value represents the principal amount that the borrower must repay. Understanding Face Value enables accountants, investors, and other stakeholders to make informed decisions regarding loan or investment valuation and risk assessment.

Sale Price

Within the context of straight line discount amortization, “Sale Price” holds significant importance as the price at which a loan or investment is sold. It serves as the basis for calculating the discount, which is amortized over the life of the loan or investment. Understanding the concept of Sale Price is crucial for accurate amortization calculations.

- Transaction Price

Sale Price represents the actual price at which a loan or investment is sold in the market. It may differ from the Face Value, resulting in either a discount or premium. The difference between the Face Value and the Sale Price forms the basis for discount amortization.

- Market Conditions

Sale Price is heavily influenced by prevailing market conditions, such as interest rates and economic outlook. Favorable market conditions may lead to a Sale Price higher than the Face Value, while unfavorable conditions may result in a Sale Price below the Face Value.

- Negotiation

In certain scenarios, the Sale Price may be subject to negotiation between the issuer and the investor. Factors such as creditworthiness of the issuer, demand for the loan or investment, and prevailing market conditions influence the negotiated Sale Price.

- Implications for Amortization

The Sale Price directly impacts the calculation of discount amortization. A lower Sale Price results in a larger discount, which is amortized over the life of the loan or investment. This affects the carrying value of the loan or investment on the issuer’s balance sheet.

In summary, Sale Price plays a critical role in straight line discount amortization by determining the discount to be amortized. Factors such as transaction price, market conditions, negotiation, and implications for amortization highlight the importance of understanding Sale Price in the context of loan and investment valuation.

Discount

Within the context of “how to calculate straight line discount amortization”, “Discount” holds significant importance as the difference between the Face Value and the Sale Price of a loan or investment. It represents the amount by which the Sale Price falls below the Face Value, resulting in a lower initial value for the issuer.

Discount plays a critical role in straight line discount amortization, as it forms the basis for calculating the amortization amount. A larger discount leads to a higher amortization expense, which in turn reduces the carrying value of the loan or investment over its lifetime. Understanding the concept of Discount is crucial for accurate amortization calculations and maintaining proper financial records.

Real-life examples of Discount can be found in various financial transactions. For instance, when a company issues bonds at a price below their Face Value, the difference represents a discount. Similarly, when a bank provides a loan at an interest rate below the market rate, the difference between the market rate and the loan rate can be considered a discount.

The practical applications of understanding Discount in straight line discount amortization are far-reaching. It enables accountants and financial analysts to accurately value loans and investments, assess the impact of discounts on financial statements, and make informed decisions regarding investment strategies. By considering the Discount, stakeholders can gain a clearer picture of the true cost of borrowing or investing.

Amortization Period

Amortization Period stands as a critical component of “how to calculate straight line discount amortization”. It directly influences the calculation and subsequent amortization of the discount over the life of a loan or investment. Understanding the relationship between Amortization Period and discount amortization is essential for accurate financial reporting and analysis.

The Amortization Period determines the number of periods over which the discount is spread. A longer Amortization Period results in a lower amortization expense in each period, leading to a more gradual reduction in the carrying value of the loan or investment. Conversely, a shorter Amortization Period results in a higher amortization expense in each period, resulting in a more rapid reduction in the carrying value.

In the context of real-life examples, consider a 5-year loan with a $100 discount and an Amortization Period of 5 years. Using straight line discount amortization, the annual amortization expense would be $20 (Discount / Amortization Period). Alternatively, if the Amortization Period were 10 years, the annual amortization expense would be $10, resulting in a slower reduction in the carrying value of the loan.

Understanding the practical applications of Amortization Period empowers accountants, financial analysts, and other stakeholders to make informed decisions regarding loan and investment valuation. It allows for accurate financial reporting, assessment of the impact of discounts on financial statements, and development of effective investment strategies. In summary, Amortization Period plays a vital role in “how to calculate straight line discount amortization”, affecting the pace and pattern of discount amortization and providing valuable insights for financial decision-making.

Amortization Rate

The Amortization Rate holds significant importance in the context of “how to calculate straight line discount amortization”. It serves as a critical component, directly influencing the calculation and subsequent amortization of the discount over the life of a loan or investment. By examining the various facets of the Amortization Rate, we gain a deeper comprehension of its role and practical applications.

- Calculation Formula

The Amortization Rate is calculated by dividing the Discount by the Amortization Period. This formula establishes the rate at which the discount is amortized in each period, determining the reduction in carrying value over the loan or investment’s lifetime.

- Impact on Amortization Expense

The Amortization Rate directly affects the amortization expense recognized in each period. A higher rate results in a larger amortization expense, leading to a more rapid reduction in the carrying value. Conversely, a lower rate results in a smaller amortization expense, resulting in a more gradual reduction in the carrying value.

- Financial Statement Presentation

The Amortization Rate influences the presentation of the discount amortization in financial statements. Under straight line discount amortization, the discount is amortized evenly over the Amortization Period, resulting in a consistent reduction in the carrying value. This consistent amortization is reflected in the financial statements.

- Implications for Investment Decisions

Understanding the Amortization Rate is essential for making informed investment decisions. Investors need to consider the impact of the amortization rate on the investment’s cash flows and overall return. A higher amortization rate may lead to higher upfront expenses, while a lower amortization rate may result in lower upfront expenses but a higher carrying value later on.

In summary, the Amortization Rate plays a vital role in “how to calculate straight line discount amortization”. It influences the amortization expense, financial statement presentation, and investment decisions. By understanding the various facets of the Amortization Rate, accountants, financial analysts, and investors can make well-informed decisions and accurately assess the financial implications of loans and investments.

Carrying Value

Carrying Value plays a pivotal role in “how to calculate straight line discount amortization”. It represents the value at which a loan or investment is carried on the issuer’s balance sheet, reflecting the initial cost minus any amortization or accumulated depreciation. The calculation of Carrying Value is closely intertwined with the concept of straight line discount amortization, as the amortization process directly impacts the Carrying Value over the life of the loan or investment.

Straight line discount amortization allocates the discount on a loan or investment evenly over its lifetime. This amortization reduces the Carrying Value of the loan or investment in a consistent manner, gradually bringing it closer to its Face Value. The discount amortization expense is recognized in the income statement, reducing the net income in each period.

In real-life examples, Carrying Value is crucial for accurate financial reporting. For instance, in the case of a bond issued at a discount, the Carrying Value would be lower than the Face Value due to the initial discount. As the discount is amortized over the bond’s life, the Carrying Value gradually increases, reflecting the reduction in the discount.

Understanding the relationship between Carrying Value and “how to calculate straight line discount amortization” has practical applications in various financial contexts. It enables accountants and financial analysts to assess the financial health of a company, make informed investment decisions, and comply with accounting standards. Accurate calculation of Carrying Value ensures reliable financial reporting and enhances the transparency of financial statements.

Interest Expense

Interest Expense plays a crucial role in “how to calculate straight line discount amortization”. It represents the periodic expense incurred on a loan or investment due to the time value of money. The connection between Interest Expense and straight line discount amortization lies in the fact that the latter is a method of allocating the discount on a loan or investment over its lifetime, affecting the Interest Expense recognized in each period.

In straight line discount amortization, the discount is amortized evenly over the life of the loan or investment, resulting in a consistent reduction in the Carrying Value. This reduction in Carrying Value, in turn, impacts the calculation of Interest Expense. As the Carrying Value decreases, the Interest Expense also decreases, as it is calculated as a percentage of the Carrying Value.

For example, consider a loan with a Face Value of $1,000 issued at a discount of $50. The straight line discount amortization over a 5-year period would result in an annual amortization of $10. Consequently, the Carrying Value of the loan would decrease by $10 each year, and the Interest Expense would also decrease by 10% of $10, which is $1.

Understanding the relationship between Interest Expense and straight line discount amortization is essential for accurate financial reporting and analysis. It enables accountants and financial analysts to assess the financial health of a company, make informed investment decisions, and comply with accounting standards. Accurate calculation of Interest Expense ensures reliable financial reporting and enhances the transparency of financial statements.

Effective Interest Rate

Effective Interest Rate holds a significant connection to “how to calculate straight line discount amortization”. It represents the actual annual interest rate of a loan or investment, considering both the stated interest rate and the impact of any discount or premium. Understanding the relationship between Effective Interest Rate and straight line discount amortization is crucial for accurate financial reporting and analysis.

Straight line discount amortization allocates the discount on a loan or investment evenly over its lifetime, affecting the Effective Interest Rate. The discount reduces the Carrying Value of the loan or investment, which in turn lowers the interest expense recognized each period. As a result, the Effective Interest Rate, which is calculated as the interest expense divided by the Carrying Value, will be lower than the stated interest rate.

For example, consider a loan with a Face Value of $1,000, a stated interest rate of 10%, and issued at a discount of $50. The straight line discount amortization over a 5-year period would result in an annual amortization of $10. This would reduce the Carrying Value of the loan each year, leading to a lower interest expense and, consequently, a lower Effective Interest Rate.

Understanding the relationship between Effective Interest Rate and straight line discount amortization is essential for various practical applications. It enables accountants and financial analysts to assess the true cost of borrowing or investing, make informed investment decisions, and comply with accounting standards. Accurate calculation of Effective Interest Rate ensures reliable financial reporting and enhances the transparency of financial statements.

Present Value

Present Value plays a critical role in “how to calculate straight line discount amortization” as it represents the current value of a future sum of money, discounted at a specified interest rate. The connection between Present Value and straight line discount amortization lies in the fact that the discount on a loan or investment is calculated based on the difference between the Face Value and the Present Value of the future cash flows.

When a loan or investment is issued at a discount, the Present Value of the future cash flows is less than the Face Value. This discount is then amortized over the life of the loan or investment using the straight line method, resulting in a consistent reduction in the Carrying Value. The Present Value is a critical component of this calculation as it determines the initial discount and, consequently, the amount of amortization expense recognized in each period.

For example, consider a 5-year loan with a Face Value of $1,000 and an annual interest rate of 10%. If the Present Value of the future cash flows is $950, the discount would be $50. Using straight line discount amortization, the annual amortization expense would be $10 ($50 discount 5 years). This would reduce the Carrying Value of the loan by $10 each year, reflecting the gradual recognition of the discount.

Understanding the relationship between Present Value and straight line discount amortization is essential for various practical applications, including financial planning, investment analysis, and accounting. It enables accountants and financial analysts to accurately value loans and investments, assess the impact of discounts on financial statements, and make informed decisions regarding investment strategies. By considering the Present Value, stakeholders can gain a clearer picture of the true cost of borrowing or investing.

Frequently Asked Questions on Straight Line Discount Amortization

This section addresses common questions and clarifies aspects related to “how to calculate straight line discount amortization”:

Question 1: What is straight line discount amortization?

Answer: Straight line discount amortization is a method of allocating the discount on a loan or investment evenly over its lifetime, reducing the carrying value consistently.

Question 2: How is the discount calculated?

Answer: The discount is calculated as the difference between the face value and the present value of the future cash flows.

Question 3: What is the amortization rate?

Answer: The amortization rate is the discount divided by the amortization period, determining the portion of the discount amortized in each period.

Question 4: How does straight line discount amortization affect the carrying value?

Answer: Straight line discount amortization reduces the carrying value of the loan or investment consistently over its lifetime.

Question 5: What is the impact on interest expense?

Answer: As the carrying value decreases, the interest expense also decreases, since it is calculated as a percentage of the carrying value.

Question 6: How is straight line discount amortization presented in financial statements?

Answer: The discount amortization is recognized as an expense in the income statement, reducing the net income in each period.

These FAQs provide a concise overview of key concepts and their practical applications. Understanding these concepts is crucial for accurate calculation and analysis of straight line discount amortization.

In the following section, we will delve into advanced applications and considerations for this amortization method within accounting frameworks.

Tips for Calculating Straight Line Discount Amortization

This section provides actionable tips to enhance your understanding and accurate calculation of straight line discount amortization:

Tip 1: Accurately Determine the Discount

Correctly calculate the discount as the difference between the face value and the present value of future cash flows to ensure precise amortization.

Tip 2: Calculate the Amortization Rate

Divide the discount by the amortization period to determine the amortization rate, which dictates the consistent reduction in carrying value.

Tip 3: Establish an Amortization Schedule

Create a schedule outlining the amortization amount for each period, providing a clear roadmap for reducing the carrying value.

Tip 4: Consider the Impact on Interest Expense

Recognize that straight line discount amortization affects interest expense, as it reduces the carrying value and, consequently, the interest calculation base.

Tip 5: Reflect Accurately in Financial Statements

Ensure proper presentation of discount amortization as an expense in the income statement, reducing net income in each period.

Tip 6: Utilize Technology for Efficiency

Employ accounting software or calculators to automate calculations, enhancing accuracy and saving time.

These tips empower you to confidently calculate straight line discount amortization, ensuring accurate financial reporting and decision-making.

In the concluding section, we will explore advanced applications and considerations for straight line discount amortization, building upon these foundational tips.

Conclusion

This comprehensive exploration of “how to calculate straight line discount amortization” has elucidated the intricacies of this amortization method. We have examined the key concepts, including discount calculation, amortization rate determination, and its impact on carrying value and financial statements.

Central to understanding straight line discount amortization is the even allocation of the discount over the loan or investment’s lifetime. This consistent reduction in carrying value aligns with the gradual recognition of the discount’s impact on the loan’s effective interest rate.

Accurate calculation of straight line discount amortization is pivotal for reliable financial reporting, informed investment decisions, and compliance with accounting standards. By comprehending the nuances of this amortization method, accountants, financial analysts, and investors can navigate the complexities of loan and investment valuation with confidence.