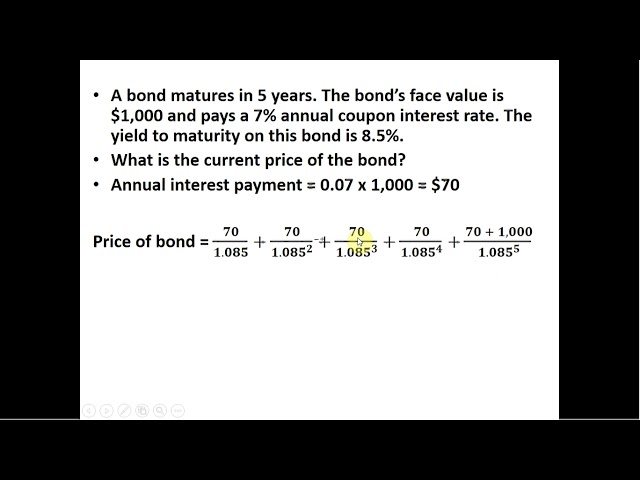

Calculating bond discounts, the difference between a bond’s face value and purchase price, is crucial in finance. Real-world scenarios exist where bonds are sold for less than their face value, and calculating the bond discount is imperative.

Bond discount calculations are significant for investors and analysts. Understanding this concept helps assess potential opportunities, evaluate risk, and make informed decisions. Historically, the concept of bond discounts was influenced by economic factors that shaped fixed-income markets.

This article aims to provide a comprehensive guide on calculating bond discounts, exploring their implications, and offering practical examples to facilitate understanding.

How to Calculate the Bond Discount

Calculating the bond discount, the difference between a bond’s face value and purchase price, involves several key aspects:

- Bond Indenture

- Coupon Rate

- Current Yield

- Maturity Date

- Face Value

- Market Price

- Discount Rate

- Time to Maturity

These aspects are interconnected. The bond indenture outlines the terms of the bond, including the coupon rate, maturity date, and face value. The current yield and market price reflect current market conditions. The discount rate is used to determine the present value of the bond’s future cash flows. Understanding these aspects is essential for accurately calculating the bond discount, which can impact investment decisions and portfolio management strategies.

Bond Indenture

A bond indenture holds utmost significance in the context of calculating bond discounts. It serves as a comprehensive legal document outlining the terms and conditions governing a bond issuance. The indenture stipulates crucial details such as the coupon rate, maturity date, and face value, which are pivotal factors in bond discount calculations.

The bond indenture acts as the cornerstone upon which bond discount calculations are based. Without this legal framework, determining the discount accurately would be impossible. Real-life examples abound, demonstrating the practical applications of bond indentures. For instance, consider a bond with a face value of $1,000, a coupon rate of 5%, and a maturity date of 10 years. If this bond is currently trading at $950 in the market, the bond discount can be calculated using the information provided in the bond indenture.

Understanding the relationship between bond indenture and bond discount calculation empowers investors and analysts to make informed decisions. It enables them to assess the potential risks and rewards associated with bond investments, evaluate the impact of market conditions on bond prices, and optimize their investment strategies. Moreover, this understanding facilitates accurate financial reporting and ensures compliance with regulatory requirements, contributing to the stability and integrity of financial markets.

Coupon Rate

The coupon rate on a bond plays a crucial role in calculating the bond discount. It represents the annual interest payment made to bondholders as a percentage of the bond’s face value. The coupon rate is a critical component in determining the bond’s present value and, consequently, its discount. A higher coupon rate generally leads to a lower bond discount, as the bond’s present value is increased by the higher periodic interest payments.

For instance, consider two bonds with a face value of $1,000 and a maturity date of 10 years. Bond A has a coupon rate of 5%, while Bond B has a coupon rate of 8%. Assuming both bonds are currently trading at $950, Bond A will have a higher bond discount than Bond B. This is because the present value of Bond A’s future cash flows is lower due to the lower coupon rate.

Understanding the connection between coupon rate and bond discount calculation empowers investors and analysts to make informed decisions. By considering the impact of coupon rate on bond pricing, they can optimize their investment strategies and effectively manage their portfolios. This understanding also plays a vital role in financial reporting and regulatory compliance, ensuring the accuracy and integrity of financial markets.

Current Yield

Current Yield (CY) is a crucial concept in the context of bond discount calculations. It represents the annual interest earned on a bond relative to its current market price. CY is inversely related to bond discount, meaning a higher CY generally leads to a lower bond discount and vice versa. This relationship stems from the fact that CY reflects the bond’s attractiveness to investors; a higher CY makes the bond more desirable, resulting in a higher market price and, consequently, a lower bond discount.

For instance, consider two bonds with a face value of $1,000 and a maturity date of 10 years. Bond A has a coupon rate of 5% and is currently trading at $950, resulting in a bond discount of $50. Bond B also has a coupon rate of 5% but is currently trading at $975, resulting in a bond discount of $25. The higher CY of Bond B ($5.13%) compared to Bond A ($5.26%) makes it more attractive to investors, leading to a higher market price and a lower bond discount.

Understanding the relationship between CY and bond discount calculation is critical for investors and analysts. It enables them to assess the attractiveness of bonds, make informed investment decisions, and optimize their portfolio strategies. Moreover, this understanding plays a vital role in financial reporting and regulatory compliance, ensuring the accuracy and integrity of financial markets.

Maturity Date

Maturity date is a pivotal aspect of bond discount calculations, as it directly influences the bond’s present value and, consequently, its discount. Understanding the nuances of maturity date is crucial for accurately determining bond discounts and making informed investment decisions.

- Time to Maturity: This refers to the duration from the date of purchase to the maturity date of the bond. A longer time to maturity generally leads to a higher bond discount, as the present value of the bond’s future cash flows is discounted over a more extended period.

- Coupon Payments: Maturity date determines the number of coupon payments the bondholder will receive. Bonds with longer maturities typically have more coupon payments, which can impact the bond’s present value and, therefore, its discount.

- Interest Rate Risk: Bonds with longer maturities are more sensitive to interest rate changes. If interest rates rise, the present value of the bond’s future cash flows decreases, leading to a wider bond discount.

- Call Feature: Some bonds have a call feature, which allows the issuer to redeem the bond before its maturity date. The presence of a call feature can affect the bond’s discount, as it introduces uncertainty regarding the bond’s actual maturity.

In summary, the maturity date of a bond is a critical factor in bond discount calculations. It influences the present value of the bond’s future cash flows, the number of coupon payments, interest rate risk, and the potential impact of call features. Understanding these aspects enables investors and analysts to accurately calculate bond discounts and make informed investment decisions.

Face Value

Comprehending the concept of “Face Value” is crucial in the context of calculating bond discounts. It represents the principal amount of a bond, serving as a benchmark against which the bond’s market price is compared.

- Nominal Value: The face value of a bond is also known as its nominal value, indicating the amount the bondholder will receive upon maturity.

- Bond Issuance: When a bond is issued, its face value determines the amount of funds the issuer receives from investors.

- Maturity Date: The face value represents the amount payable to the bondholder on the bond’s maturity date, assuming no defaults.

- Bond Discount Calculation: The difference between a bond’s face value and its market price is the bond discount. A bond is said to be trading at a discount when its market price is below its face value.

Understanding these facets of face value empowers investors and analysts to accurately calculate bond discounts, assess the relative value of bonds, and make informed investment decisions. By considering the face value in conjunction with other bond characteristics such as coupon rate and maturity date, they can effectively evaluate the potential returns and risks associated with bond investments.

Market Price

Market Price plays a key role in calculating bond discounts, as it directly influences the discount’s magnitude and implications. Several facets of Market Price are worth considering in this context:

- Current Market Conditions: The prevailing market conditions, such as economic outlook, interest rate environment, and investor sentiment, can significantly impact bond prices. A bond’s Market Price may fluctuate based on these factors, affecting the discount calculation.

- Supply and Demand: The forces of supply and demand in the bond market can influence Market Price. When there is high demand for a particular bond, its Market Price may rise, leading to a lower bond discount. Conversely, low demand can result in a lower Market Price and a wider discount.

- Creditworthiness of Issuer: The Market Price of a bond is influenced by the creditworthiness of the issuer. Bonds issued by entities with higher credit ratings tend to have higher Market Prices, resulting in lower bond discounts, as investors perceive them as less risky.

- Maturity Date: The Market Price of a bond is also affected by its maturity date. Bonds with longer maturities typically have higher Market Prices compared to those with shorter maturities, leading to narrower bond discounts. This is because investors demand a higher return for locking their funds for a more extended period.

In summary, the Market Price of a bond is a dynamic factor influenced by various elements, including current market conditions, supply and demand, issuer creditworthiness, and maturity date. Understanding these facets is crucial for accurately calculating bond discounts and making informed investment decisions.

Discount Rate

Within the framework of calculating bond discounts, the Discount Rate holds immense significance in determining the bond’s present value and, consequently, the magnitude of the discount. Various facets of the Discount Rate influence its impact on bond discount calculations.

- Market Interest Rates: The Discount Rate is often aligned with prevailing market interest rates. Higher market interest rates typically lead to higher Discount Rates, resulting in lower bond prices and wider bond discounts.

- Time to Maturity: The Discount Rate also considers the time to maturity of the bond. Bonds with longer maturities generally demand higher Discount Rates to compensate investors for the extended period of investment.

- Credit Risk: The perceived credit risk associated with the bond issuer can influence the Discount Rate. Bonds issued by entities with lower credit ratings may require higher Discount Rates to account for the increased risk of default, leading to wider bond discounts.

- Inflation Expectations: Inflation expectations can impact the Discount Rate. Anticipated inflation may warrant higher Discount Rates to protect investors from the eroding effects of inflation on the bond’s future cash flows.

In summary, the Discount Rate plays a crucial role in bond discount calculations, incorporating factors such as market interest rates, time to maturity, credit risk, and inflation expectations. Understanding these facets enables investors and analysts to accurately determine bond discounts and make informed investment decisions.

Time to Maturity

In the context of calculating bond discounts, Time to Maturity emerges as a pivotal factor, influencing the discount’s magnitude and the overall investment strategy. Time to Maturity refers to the duration between the bond’s issuance and its maturity date, which directly impacts the present value of the bond’s future cash flows. A longer Time to Maturity translates to a higher present value due to the compounding effect of interest over an extended period. Consequently, this leads to a narrower bond discount.

The significance of Time to Maturity in calculating bond discounts stems from the fact that longer maturities entail greater uncertainty and risk. Investors demand higher returns for committing their funds over extended periods, which is reflected in the wider bond discounts associated with longer maturities. Moreover, bonds with longer maturities are more sensitive to interest rate fluctuations, making their present values more susceptible to changes in the market environment.

Real-life examples abound, showcasing the practical applications of Time to Maturity in bond discount calculations. Consider two bonds with identical face values and coupon rates but varying maturities. The bond with a longer maturity will typically have a higher present value and, therefore, a narrower bond discount. This is because the present value of its future cash flows is spread over a more extended period, resulting in a lower effective interest rate.

Understanding the relationship between Time to Maturity and bond discount calculations empowers investors and analysts to make informed decisions. By incorporating Time to Maturity into their calculations, they can accurately assess the value of bonds, compare investment options, and manage their portfolios effectively. Moreover, this understanding is crucial in financial reporting and regulatory compliance, ensuring accurate bond valuations and transparent financial markets.

Bond Discount Calculation FAQs

This section addresses common questions and clarifications related to calculating bond discounts, providing concise and informative answers.

Question 1: What is the formula for calculating bond discount?

Answer: Bond Discount = Face Value – Purchase Price

Question 2: How does the coupon rate affect bond discount?

Answer: A higher coupon rate generally leads to a lower bond discount, as the present value of future interest payments is higher.

Question 3: What is the impact of time to maturity on bond discount?

Answer: Longer maturities typically result in higher bond discounts due to the present value of cash flows being spread over a more extended period.

Question 4: How is bond discount accounted for in financial statements?

Answer: Bond discount is amortized over the bond’s life, reducing the carrying value of the bond and increasing interest expense.

Question 5: Can a bond be purchased at a premium instead of a discount?

Answer: Yes, a bond can trade at a premium if its market price exceeds its face value, resulting in a bond premium.

Question 6: What are the implications of bond discounts for investors?

Answer: Bond discounts can provide investors with opportunities to acquire bonds at a lower cost, potentially leading to higher returns upon maturity.

These FAQs provide a concise overview of key considerations in bond discount calculations, offering a foundation for further exploration into bond valuation and investment strategies.

In the next section, we delve deeper into the practical applications of bond discount calculations, examining real-world examples and discussing advanced concepts for bond portfolio management.

Bond Discount Calculation Tips

Applying these practical tips can enhance the accuracy and effectiveness of bond discount calculations, leading to informed investment decisions.

Tip 1: Determine the Bond’s Face Value and Purchase Price: Clearly identify the face value, which represents the principal amount, and the purchase price, which reflects the current market value.

Tip 2: Calculate the Bond’s Coupon Payments: Determine the periodic interest payments based on the coupon rate and face value.

Tip 3: Estimate the Bond’s Time to Maturity: Calculate the duration from the purchase date to the maturity date, considering any potential call or put options.

Tip 4: Select an Appropriate Discount Rate: Choose a discount rate that aligns with the bond’s credit risk, market conditions, and time to maturity.

Tip 5: Utilize a Bond Discount Calculator: Leverage online tools or financial calculators specifically designed for bond discount calculations.

Tip 6: Consider the Impact of Taxes: Factor in the tax implications of bond discounts, as they may affect the overall investment return.

By following these tips, investors and analysts can refine their bond discount calculations, leading to more precise valuations and informed investment strategies.

In the concluding section, we will explore advanced concepts in bond discount calculations, delving into complex scenarios and techniques for effective bond portfolio management.

Conclusion

Throughout this article, we have explored the intricacies of calculating bond discounts, shedding light on the crucial factors and techniques involved in this process. Key insights have emerged, including the inverse relationship between bond discounts and coupon rates, the impact of time to maturity on discount calculations, and the significance of the discount rate in determining the present value of future cash flows.

Understanding bond discount calculations empowers investors and analysts to make informed investment decisions. It enables them to assess the relative value of bonds, compare investment options, and manage their portfolios effectively. This understanding is also crucial in financial reporting and regulatory compliance, ensuring accurate bond valuations and transparent financial markets.