Zero coupon bond calculation is the process of determining the present value of a bond that pays no periodic interest payments (coupons), using a financial calculator or spreadsheet program like Microsoft Excel. This method is crucial for investors looking to evaluate the value of these types of bonds, which offer a single payment at maturity.

Understanding how to calculate zero coupon bonds in Excel holds significant relevance in financial markets. Zero coupon bonds are often used as building blocks for more complex financial instruments and serve as benchmarks for interest rate expectations. Historically, the development of the Black-Scholes model marked a key advancement in the pricing of zero coupon bonds, revolutionizing fixed income markets.

In this article, we will delve into the intricacies of calculating zero coupon bonds in Excel, providing step-by-step instructions, exploring practical applications, and discussing the factors that influence their valuation.

How to Calculate Zero Coupon Bond in Excel

Calculating zero coupon bonds in Excel is a critical skill in fixed income analysis. Key aspects involved include:

- Present value

- Maturity date

- Yield to maturity

- Face value

- Excel functions (PV, RATE)

- Financial modeling

- Bond valuation

- Investment analysis

Understanding these aspects allows for accurate calculation of zero coupon bond values, enabling informed investment decisions. The Excel PV function discounts future cash flows to determine present value, while the RATE function calculates yield to maturity. Financial modeling incorporates these calculations to assess bond performance and make informed investment choices.

Present value

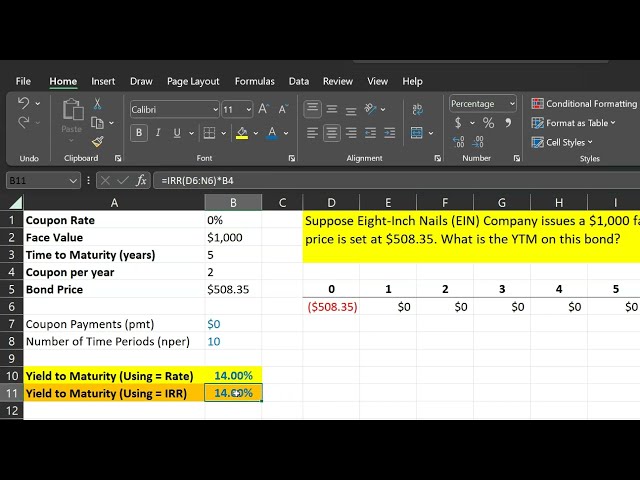

Present value (PV) is a critical component in calculating the value of zero coupon bonds in Excel. Zero coupon bonds make a single payment at maturity, and their value is determined by discounting the future payment back to the present using the present value formula: PV = FV / (1 + r)n where: – PV is the present value – FV is the future value (face value of the bond) – r is the yield to maturity (YTM) – n is the number of periods to maturity

In the context of zero coupon bonds, the future value is known (face value), and the yield to maturity is either given or can be estimated using Excel’s RATE function. By manipulating the PV formula in Excel, we can solve for the yield to maturity, which is a key metric in bond valuation.

Understanding the relationship between present value and zero coupon bond calculation is essential for accurate bond valuation. It allows investors to assess the fair value of zero coupon bonds, compare them to other fixed income investments, and make informed investment decisions. Furthermore, this understanding has practical applications in financial modeling, portfolio management, and risk analysis.

Maturity date

In the context of zero coupon bonds, the maturity date is the date on which the bond matures and the face value is paid to the bondholder. It is a crucial factor in calculating the present value and yield to maturity of a zero coupon bond using Excel.

- Date of Payment: The maturity date determines the date on which the bondholder receives the face value of the bond, which is the only payment for zero coupon bonds.

- Bond Pricing: The maturity date influences the present value calculation of the bond. Bonds with longer maturities generally have lower present values compared to those with shorter maturities, assuming the same yield to maturity.

- Yield to Maturity Calculation: The maturity date is used in conjunction with the present value and face value to calculate the yield to maturity, which is the internal rate of return (IRR) of the bond.

- Investment Strategy: Investors consider the maturity date when making investment decisions. Bonds with different maturity dates have varying risk and return profiles, which align with different investment strategies and time horizons.

Understanding the significance of the maturity date enables accurate calculation of zero coupon bond values in Excel. This knowledge empowers investors to make informed decisions regarding bond investments, assess the impact of maturity on bond pricing, and tailor their investment strategies accordingly.

Yield to Maturity

In the context of “how to calculate zero coupon bond in excel”, yield to maturity (YTM) plays a pivotal role. It represents the annual rate of return an investor can expect to earn by holding a zero coupon bond until maturity. Understanding YTM is essential for accurate bond valuation using Excel.

- Bond Pricing: YTM is a key factor in determining the present value of a zero coupon bond in Excel. Bonds with higher YTMs have lower present values, and vice versa.

- Investment Decision: YTM allows investors to compare the expected returns of different zero coupon bonds and make informed investment decisions.

- Risk Assessment: YTM reflects the market’s perception of the bond’s risk. Higher YTMs may indicate higher perceived risk.

By considering these facets of yield to maturity, investors can effectively calculate and analyze the value of zero coupon bonds in Excel, enabling them to make informed investment choices and manage their fixed income portfolios.

Face value

In the context of calculating zero coupon bonds in Excel, face value holds significant importance. Face value, also known as par value or maturity value, represents the principal amount that the bondholder receives upon the bond’s maturity. It is a critical component in determining the present value and yield to maturity of a zero coupon bond.

The face value directly influences the calculation of a zero coupon bond’s present value in Excel. The present value formula, PV = FV / (1 + r)^n, shows that the present value is inversely proportional to the face value. This implies that bonds with higher face values have higher present values, assuming the same yield to maturity and maturity date.

Real-life examples further illustrate this relationship. Consider two zero coupon bonds with the same yield to maturity and maturity date, but different face values. The bond with a higher face value would have a higher present value, simply because it represents a larger future cash flow. This understanding is crucial for investors to accurately assess the value of zero coupon bonds.

Practically, this understanding allows investors to make informed investment decisions. By considering the face value in conjunction with other factors such as yield to maturity and maturity date, investors can compare the relative value of different zero coupon bonds and select those that best align with their investment goals and risk tolerance.

Excel functions (PV, RATE)

In the context of “how to calculate zero coupon bond in excel”, Excel functions (PV, RATE) play a pivotal role. These functions provide a structured and efficient approach to valuing zero coupon bonds, which are fixed income securities that pay no periodic interest payments and return the principal amount at maturity.

The PV function, or Present Value function, calculates the present value of a future cash flow, which is essential in determining the fair value of a zero coupon bond. By discounting the face value of the bond back to the present using the specified yield to maturity, the PV function enables investors to assess the bond’s attractiveness relative to other investment opportunities.

Complementing the PV function, the RATE function, or Interest Rate function, calculates the yield to maturity of a zero coupon bond. Yield to maturity represents the annualized rate of return an investor can expect to earn by holding the bond until its maturity date. Using the RATE function, investors can determine the implied yield based on the bond’s present value, face value, and maturity date, providing valuable insights into the bond’s risk and return profile.

The practical applications of these Excel functions are far-reaching. Financial analysts and portfolio managers utilize these functions to evaluate and compare zero coupon bonds, make informed investment decisions, and manage fixed income portfolios effectively. Furthermore, understanding the functionality of PV and RATE functions empowers investors to perform sensitivity analysis, assess the impact of changing market conditions on bond values, and make data-driven investment choices.

In summary, Excel functions (PV, RATE) are indispensable tools for calculating zero coupon bond values in excel. Their ability to determine present value and yield to maturity provides a comprehensive analytical framework for investors seeking to navigate the fixed income markets.

Financial modeling

Financial modeling holds a central position in the context of “how to calculate zero coupon bond in excel”. It serves as the backbone for intricate calculations and financial analysis, enabling the evaluation and valuation of zero coupon bonds.

As a critical component of “how to calculate zero coupon bond in excel”, financial modeling provides an organized framework to incorporate essential factors such as present value, yield to maturity, face value, and maturity date. This structured approach ensures accuracy and efficiency in calculating zero coupon bond values, empowering informed decision-making for investors and financial professionals.

In practical terms, financial modeling allows for the development of dynamic spreadsheets that can accommodate various scenarios and assumptions. By simulating different market conditions and interest rate environments, investors can assess the potential impact on zero coupon bond values, enabling proactive portfolio management strategies.

In summary, financial modeling serves as an indispensable tool in “how to calculate zero coupon bond in excel”. Its structured approach, ability to incorporate key factors, and practical applications provide a solid foundation for accurate bond valuation and informed investment decisions.

Bond valuation

In the realm of “how to calculate zero coupon bond in excel”, understanding bond valuation is paramount. Bond valuation serves as the foundation for determining the fair value of a zero coupon bond, enabling investors and financial professionals to make informed decisions. Without accurate bond valuation, calculating zero coupon bond values in Excel would be rendered ineffective.

Bond valuation involves several key factors, including present value, yield to maturity, face value, and maturity date. By incorporating these factors into Excel calculations, investors can accurately assess the intrinsic value of zero coupon bonds and make informed investment choices. Zero coupon bonds, unlike traditional coupon bonds, do not pay periodic interest payments, making their valuation heavily reliant on accurate present value calculations.

Real-life examples further solidify the connection between bond valuation and “how to calculate zero coupon bond in excel”. Consider an investor evaluating two zero coupon bonds with the same maturity date but different face values. Using Excel, the investor can calculate the present value of each bond using the PV function, incorporating the specified yield to maturity and maturity date. The bond with the higher face value will have a higher present value, reflecting its larger future cash flow upon maturity.

In summary, bond valuation and “how to calculate zero coupon bond in excel” are inextricably linked. Bond valuation provides the theoretical framework and essential factors for calculating zero coupon bond values in Excel. Understanding this connection empowers investors to make well-informed investment decisions, manage their fixed income portfolios effectively, and navigate the complexities of bond markets.

Investment analysis

Investment analysis is a critical component of “how to calculate zero coupon bond in excel”. It provides a structured framework for evaluating the intrinsic value and potential returns of zero coupon bonds, enabling investors to make informed investment decisions. Without a thorough understanding of investment analysis, calculating zero coupon bond values in Excel would lack context and accuracy.

Real-life examples illustrate the practical applications of this understanding. Consider an investment analyst tasked with evaluating a portfolio of zero coupon bonds. Using Excel, the analyst can calculate the present value of each bond, incorporating yield to maturity, face value, and maturity date. This analysis provides valuable insights into the fair value of the bonds and their potential contribution to the overall portfolio’s risk and return profile.

Furthermore, investment analysis allows investors to assess the impact of changing market conditions and interest rate scenarios on zero coupon bond values. By incorporating dynamic assumptions into Excel models, investors can simulate different market environments and evaluate the potential impact on their bond investments. This forward-looking analysis empowers investors to make proactive portfolio adjustments and mitigate potential risks.

In summary, investment analysis and “how to calculate zero coupon bond in excel” are closely intertwined. Investment analysis provides the theoretical foundation and analytical framework for calculating zero coupon bond values accurately. This understanding enables investors to make well-informed investment decisions, manage their fixed income portfolios effectively, and navigate the complexities of bond markets.

Frequently Asked Questions

This section addresses common queries and clarifies various aspects of “how to calculate zero coupon bond in excel” to enhance your understanding.

Question 1: What is the significance of yield to maturity (YTM) in calculating zero coupon bond value?

Answer: Yield to maturity (YTM) is a critical factor that determines the present value of a zero coupon bond. A higher YTM results in a lower present value, and vice versa. It represents the annualized rate of return an investor can expect to earn by holding the bond until maturity.

Question 2: How does the maturity date impact the calculation of zero coupon bond value?

Answer: The maturity date is the date on which the bond matures and the face value is paid. Bonds with longer maturities generally have lower present values compared to those with shorter maturities, assuming the same YTM, due to the time value of money.

Question 3: What is the relationship between face value and zero coupon bond value?

Answer: Face value represents the amount paid to the bondholder at maturity. It directly influences the present value of a zero coupon bond, with higher face values resulting in higher present values, assuming the same YTM and maturity date.

Question 4: How can I use Excel functions to calculate zero coupon bond values?

Answer: Excel provides functions like PV (Present Value) and RATE (Interest Rate) to calculate zero coupon bond values. The PV function calculates the present value based on the face value, YTM, and maturity date, while the RATE function calculates the YTM based on the present value, face value, and maturity date.

Question 5: What is the practical significance of calculating zero coupon bond values?

Answer: Calculating zero coupon bond values enables investors to assess the fair value of these bonds and make informed investment decisions. It helps them compare different bonds, evaluate their risk and return profiles, and manage fixed income portfolios effectively.

Question 6: Are there any limitations to calculating zero coupon bond values in Excel?

Answer: While Excel provides valuable tools for calculating zero coupon bond values, it may have limitations in handling complex bond structures or incorporating advanced valuation models. For such scenarios, specialized financial calculators or software may be necessary.

These FAQs provide essential insights into the intricacies of calculating zero coupon bond values in Excel. Understanding these concepts empowers investors and financial professionals to make well-informed investment decisions and navigate the fixed income markets effectively.

In the next section, we will delve into advanced topics related to zero coupon bond valuation, exploring yield curve analysis and the impact of interest rate changes on bond values.

Tips for Efficiently Calculating Zero Coupon Bond Values in Excel

To enhance the accuracy and efficiency of zero coupon bond calculations in Excel, consider implementing the following actionable tips:

Tip 1: Utilize Excel Functions: Leverage Excel’s built-in functions, such as PV (Present Value) and RATE (Interest Rate), to automate calculations and minimize manual errors.

Tip 2: Construct Dynamic Spreadsheets: Create dynamic spreadsheets that allow for easy adjustment of variables like yield to maturity and maturity date, enabling quick analysis of various scenarios.

Tip 3: Validate Data Inputs: Ensure the accuracy of your calculations by implementing data validation rules to restrict invalid inputs and maintain data integrity.

Tip 4: Incorporate Sensitivity Analysis: Perform sensitivity analysis to assess the impact of changing input parameters on bond values, providing insights into potential risks and rewards.

Tip 5: Consider Amortization Schedules: For zero coupon bonds with embedded amortization features, incorporate amortization schedules to accurately reflect the gradual recognition of interest income.

Tip 6: Utilize Solver Tool: Employ Excel’s Solver tool to optimize bond values by finding the YTM that matches a desired present value or maturity value.

Tip 7: Explore VBA Macros: Enhance your Excel capabilities by creating VBA macros to automate repetitive tasks and streamline bond valuation processes.

Tip 8: Seek Professional Guidance: When dealing with complex bond structures or advanced valuation models, consider seeking guidance from financial professionals to ensure accurate results.

By implementing these tips, you can significantly improve the efficiency, accuracy, and reliability of your zero coupon bond calculations in Excel.

In the final section of this article, we will delve into the intricacies of yield curve analysis and its implications for zero coupon bond valuation.

Conclusion

In this article, we have delved into the intricacies of calculating zero coupon bond values in Excel, exploring the essential concepts and practical applications. Key insights include the significance of present value, yield to maturity, face value, and maturity date in determining bond values.

Understanding how to calculate zero coupon bond values empowers investors and financial professionals to make informed investment decisions, manage fixed income portfolios effectively, and navigate the complexities of bond markets. Accurate valuation is crucial for assessing the fair value of zero coupon bonds and comparing them to other fixed income investments.