Determining the price of a coupon bond is essential for investors seeking fixed income returns. A coupon bond represents a loan made by an investor to a corporation or government. In return, the investor receives regular interest payments (coupons) and the repayment of the principal amount upon maturity.

Understanding how to calculate coupon bond prices empowers investors to make informed decisions when purchasing or selling these securities. It allows them to assess the bond’s value relative to the current market conditions and interest rates.

The advent of electronic bond trading platforms has revolutionized the pricing process, making it more efficient and accessible for all market participants.

How to Calculate Coupon Bond Price

Understanding the nuances of coupon bond pricing enables investors to navigate the fixed income market with precision and confidence.

- Par Value

- Coupon Rate

- Maturity Date

- Yield to Maturity

- Present Value

- Accrued Interest

- Clean Price

- Dirty Price

These key aspects interplay to determine the fair value of a coupon bond. Understanding their interconnections empowers investors to make well-informed decisions, whether buying, selling, or holding these securities.

Par Value

Par value, also known as face value, serves as a crucial reference point in the valuation of coupon bonds. It signifies the principal amount that the bond issuer promises to repay upon maturity. Understanding its various facets provides a solid foundation for calculating coupon bond prices.

- Nominal Value: The par value represents the bond’s nominal or face value, which is the amount initially borrowed by the issuer.

- Maturity Amount: At maturity, the issuer is obligated to repay the par value to the bondholder, completing the loan agreement.

- Coupon Payment Calculation: The coupon rate, expressed as a percentage of the par value, determines the amount of periodic interest payments.

- Bond Market Quotation: In the bond market, prices are often quoted as a percentage of par value, providing a standardized reference point for comparing bonds with different face values.

Comprehending these aspects of par value empowers investors to accurately calculate coupon bond prices and make informed investment decisions. It serves as a cornerstone for further exploration into the complexities of bond valuation.

Coupon Rate

The coupon rate is a critical variable that significantly influences the calculation of coupon bond prices. It has various aspects that investors should comprehend to make informed decisions.

- Nominal Rate: The coupon rate is typically expressed as an annual percentage of the bond’s par value, representing the fixed interest payments the bondholder receives.

- Semi-Annual Payments: In most cases, coupon bonds make semi-annual interest payments, with the coupon rate divided by two and paid every six months.

- Market Interest Rates: The coupon rate should be viewed in relation to the prevailing market interest rates. Higher coupon rates are generally offered when market rates are low, and vice versa.

- Bond Price Impact: The coupon rate directly affects the bond’s price. Bonds with higher coupon rates tend to trade at a premium to their par value, while those with lower coupon rates may trade at a discount.

Understanding these facets of the coupon rate empowers investors to accurately calculate coupon bond prices, assess their value relative to market conditions, and make well-informed investment decisions.

Maturity Date

Maturity date plays a pivotal role in determining the price of a coupon bond. It marks the specific date when the bond issuer must repay the principal amount to the bondholder, concluding the loan agreement.

- Final Repayment: Maturity date signifies the termination of the bond’s life, when the issuer fulfills its obligation to repay the borrowed funds.

- Coupon Payment Cessation: Upon maturity, the issuer ceases making coupon payments, as the principal amount becomes due in its entirety.

- Bond Value Impact: The maturity date influences the bond’s present value and market price. Bonds with shorter maturities generally trade closer to their par value, while those with longer maturities may exhibit greater price fluctuations.

Understanding the implications of maturity date empowers investors to make informed decisions about the duration and risk profile of their bond investments. It also facilitates accurate calculations of coupon bond prices, enabling investors to evaluate potential returns and assess the value of these fixed-income securities.

Yield to Maturity

Yield to Maturity (YTM) is a crucial concept in determining the price of a coupon bond. It represents the annualized rate of return an investor can expect to receive if they hold the bond until maturity. Understanding YTM is essential for accurate coupon bond price calculations and informed investment decisions.

- Current Yield: Calculated as the annual coupon payment divided by the current market price, it provides an indication of the bond’s immediate income potential.

- Coupon Rate: The fixed percentage of the par value paid as interest payments, which directly influences the bond’s YTM.

- Time to Maturity: The period until the bond’s maturity date, which affects the present value of future cash flows and ultimately the YTM.

- Market Interest Rates: Prevailing interest rates in the market impact the YTM, as investors compare the bond’s return to alternative investment opportunities.

By considering these facets of YTM, investors can accurately calculate coupon bond prices and make informed decisions about their fixed-income investments. YTM provides a comprehensive measure of a bond’s return potential, taking into account both current income and future capital appreciation.

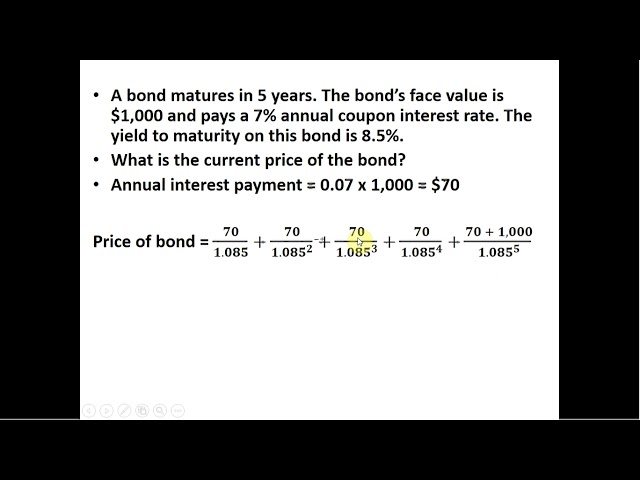

Present Value

Present Value (PV) plays a central role in determining the price of a coupon bond. It represents the current value of all future cash flows associated with the bond, including both coupon payments and the repayment of the principal at maturity. Understanding PV is essential for accurate coupon bond price calculations and informed investment decisions.

The calculation of PV in the context of coupon bond pricing involves discounting the future cash flows back to the present using an appropriate discount rate. This discount rate is typically the prevailing market interest rate or the Yield to Maturity (YTM) of the bond. By considering the time value of money, PV provides a comprehensive measure of the bond’s intrinsic value, taking into account the current worth of its future cash inflows.

In practice, PV is a critical component of various bond pricing models, including the traditional discounted cash flow (DCF) method. By accurately calculating the PV of the bond’s future cash flows, investors can determine the fair market price that reflects its intrinsic value. This understanding enables investors to make informed decisions about whether to buy, sell, or hold a particular coupon bond.

Moreover, PV has broader applications in financial analysis and investment management. It is used in the valuation of various financial instruments, such as stocks, options, and derivatives. Understanding PV empowers investors and financial professionals to make informed Entscheidungen about investment opportunities and manage their portfolios effectively.

Accrued Interest

In the context of calculating coupon bond prices, Accrued Interest represents the interest earned on a bond that has not yet been paid to the bondholder. A clear understanding of Accrued Interest is crucial for accurate bond price calculations and informed investment decisions.

- Calculation: Accrued Interest is calculated as the prorated portion of interest earned since the last coupon payment date. It is determined by multiplying the bond’s annual coupon rate by the number of days since the last payment, divided by the number of days in the coupon period.

- Bond Price Impact: Accrued Interest is added to the bond’s clean price to determine the dirty price, which represents the total cost of purchasing the bond. When buying a bond, investors are responsible for paying the accrued interest, which is then reflected in the bond’s price.

- Tax Implications: In some jurisdictions, accrued interest may be subject to taxation, affecting the overall return on the bond investment. It is important for investors to consider the tax implications of accrued interest when making investment decisions.

- Example: Consider a bond with a $1,000 face value, a 5% annual coupon rate, and a coupon payment frequency of semi-annual. If 90 days have passed since the last coupon payment, the accrued interest would be $12.50 (5% x $1,000 x 90 days / 180 days).

Understanding these facets of Accrued Interest empowers investors to make informed Entscheidungen about bond investments, accurately calculate bond prices, and assess the overall return potential of fixed-income securities.

Clean Price

Clean Price plays a pivotal role in the accurate calculation of coupon bond prices. It represents the price of the bond excluding accrued interest. Understanding the connection between Clean Price and how to calculate coupon bond price is essential for investors seeking to make informed decisions in the fixed-income market.

When calculating coupon bond prices, accrued interest must be considered as it represents the interest earned since the last coupon payment date but not yet paid to the bondholder. Clean Price is the bond’s price without this accrued interest. It serves as the base value upon which accrued interest is added to determine the Dirty Price, which represents the total cost of purchasing the bond.

Real-life examples further illustrate the connection. Consider a bond with a $1,000 face value, a 5% annual coupon rate, and a coupon payment frequency of semi-annual. If the bond is trading at a Clean Price of $980 and 90 days have passed since the last coupon payment, the accrued interest would be $12.50. In this case, the Dirty Price would be $992.50, which reflects the Clean Price plus the accrued interest.

Understanding the connection between Clean Price and coupon bond price calculation is crucial for investors as it enables them to accurately determine the true cost of the bond, factor in the time value of money, and make informed investment decisions. It empowers investors to compare bond prices across different issues and maturities, assess the potential return on their investment, and manage their fixed-income portfolios effectively.

Dirty Price

Within the context of calculating coupon bond prices, Dirty Price emerges as a critical concept that takes into account not only the bond’s Clean Price but also the accrued interest up to the settlement date. Understanding Dirty Price is pivotal for investors seeking to make informed decisions in the fixed-income market.

- Clean Price Plus Accrued Interest: Dirty Price represents the total cost of purchasing a bond, which includes the Clean Price, the bond’s price excluding accrued interest, and the accrued interest that has accumulated since the last coupon payment date.

- Real-Life Example: Consider a bond with a $1,000 face value, a 5% annual coupon rate, and a coupon payment frequency of semi-annual. If the bond is trading at a Clean Price of $980 and 90 days have passed since the last coupon payment, the accrued interest would be $12.50. In this case, the Dirty Price would be $992.50, which reflects the Clean Price plus the accrued interest.

- Relevance to Bond Pricing: Dirty Price plays a crucial role in accurate bond pricing, as it incorporates both the time value of money and the interest earned since the last coupon payment date. It provides a comprehensive measure of the bond’s market value.

- Implications for Investors: Understanding Dirty Price enables investors to compare bond prices across different issues and maturities, assess the potential return on their investment, and make informed decisions about buying, selling, or holding bonds.

In essence, Dirty Price serves as a crucial factor in calculating coupon bond prices, as it captures both the bond’s Clean Price and the accrued interest. By considering Dirty Price, investors can accurately determine the total cost of a bond investment, evaluate its potential return, and make informed decisions in the fixed-income market.

Frequently Asked Questions

This section addresses frequently asked questions related to calculating coupon bond prices, providing clarity and addressing common concerns.

Question 1: What is the formula for calculating coupon bond price?

Answer: The formula is: Bond Price = Present Value of Future Coupon Payments + Present Value of Principal Repayment.

Question 2: How do I calculate the present value of future coupon payments?

Answer: Multiply each periodic coupon payment by the present value factor corresponding to its payment date and sum the results.

Question 3: How do I calculate the present value of principal repayment?

Answer: Multiply the principal amount by the present value factor corresponding to the bond’s maturity date.

Question 4: What is the relationship between coupon rate and bond price?

Answer: Bonds with higher coupon rates generally have higher prices, as they provide a higher stream of income.

Question 5: How does the time to maturity affect bond price?

Answer: Longer-term bonds are more sensitive to changes in interest rates, and their prices fluctuate more than shorter-term bonds.

Question 6: What are the factors that influence coupon bond prices?

Answer: Coupon rate, time to maturity, prevailing interest rates, and creditworthiness of the issuer.

These FAQs provide a concise overview of the key concepts and calculations involved in determining coupon bond prices. Understanding these principles empowers investors to make informed decisions when investing in fixed-income securities.

In the next section, we will delve deeper into advanced topics related to coupon bond pricing, including the impact of yield to maturity and the different methods used to calculate bond prices.

Tips for Calculating Coupon Bond Prices

To accurately calculate coupon bond prices, consider the following practical tips:

Tip 1: Determine Key Inputs: Gather accurate data for coupon rate, time to maturity, face value, and prevailing market interest rates.

Tip 2: Calculate Present Values: Use appropriate present value factors to discount future coupon payments and the principal repayment to their present values.

Tip 3: Sum Present Values: Add the present values of all future coupon payments and the principal repayment to arrive at the bond’s price.

Tip 4: Consider Accrued Interest: For bonds purchased between coupon payment dates, add accrued interest to the bond’s price to determine the dirty price.

Tip 5: Use a Financial Calculator or Spreadsheet: Leverage technology to simplify the calculations and reduce the risk of errors.

Tip 6: Understand Market Factors: Stay informed about economic conditions and interest rate trends that can influence bond prices.

Tip 7: Compare to Market Prices: Validate your calculated bond price by referencing market data and quotations.

Tip 8: Seek Professional Advice: If needed, consult with a financial advisor or bond specialist for guidance and personalized recommendations.

Following these tips empowers you to confidently calculate coupon bond prices, assess their value, and make informed investment decisions.

In the concluding section, we will discuss advanced strategies for bond pricing, including the impact of yield to maturity and the application of various pricing models.

Conclusion

This comprehensive guide has explored the intricacies of calculating coupon bond prices, providing a thorough understanding of the key factors and methods involved. We have emphasized the importance of accurately determining present values, considering accrued interest, and incorporating market factors into the calculations.

Remember, bond pricing is a dynamic process influenced by economic conditions and interest rate fluctuations. Staying informed about market trends and seeking professional guidance when necessary can enhance your ability to make sound investment decisions. By mastering the concepts discussed in this article, you are well-equipped to navigate the fixed-income market with confidence.