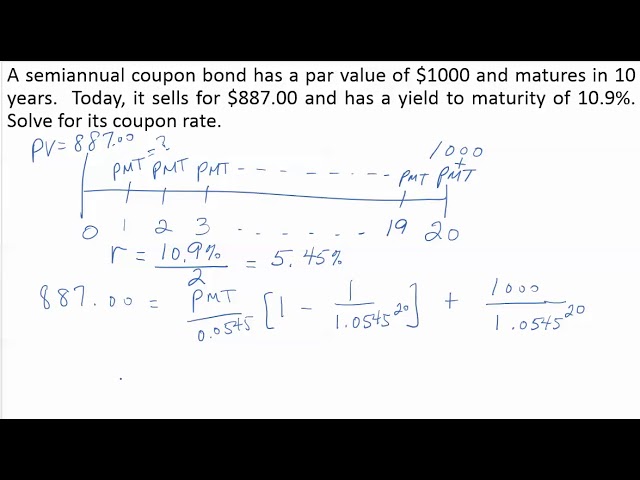

Calculating coupon payments, the periodic interest payments made on bonds, is a fundamental concept in finance. Imagine investing in a corporate bond with a $1,000 face value and a 5% annual coupon rate. Every six months, you would receive a coupon payment of $25 (5% of $1,000 divided by 2).

Understanding how to calculate coupon payments is essential for investors, analysts, and anyone involved in bond markets. It allows for accurate assessment of returns, investment decisions, and risk management.

Historically, the development of standardized bond contracts in the 19th century simplified the calculation and payment of coupons. This revolutionized bond markets and facilitated the growth of modern finance. Today, calculating coupon payments remains a crucial aspect of bond analysis and valuation.

How to Calculate Coupon Payment

Understanding how to calculate coupon payments is crucial for various aspects of bond analysis and investment. Key aspects to consider include:

- Face Value

- Coupon Rate

- Payment Frequency

- Accrual Period

- Ex-Dividend Date

- Payment Date

- Clean Price

- Dirty Price

These aspects interrelate to determine the coupon payment amount and timing. For example, the face value and coupon rate directly influence the coupon payment. The payment frequency and accrual period determine how often and over what period interest accrues. The ex-dividend date and payment date specify when the coupon payment is made and detached from the bond price. The clean and dirty prices reflect the bond’s value with and without accrued interest, respectively.

Face Value

Face value, also known as par value or nominal value, is a fundamental concept in understanding how to calculate coupon payments. It represents the principal amount borrowed by the bond issuer and repaid to the bondholder at maturity. The face value serves as the basis upon which coupon payments are calculated.

The coupon rate, expressed as a percentage of the face value, determines the amount of interest paid to the bondholder. For example, a bond with a face value of $1,000 and a 5% coupon rate would pay an annual coupon payment of $50 (5% x $1,000). Therefore, a higher face value directly translates to a higher coupon payment, assuming the coupon rate remains constant.

Understanding the relationship between face value and coupon payment is crucial for investors when evaluating bonds and making informed investment decisions. By considering the face value along with other factors such as the coupon rate and maturity date, investors can assess the potential returns and risks associated with a particular bond.

Coupon Rate

Coupon rate plays a crucial role in the calculation of coupon payments. It represents the annual interest rate paid to bondholders, expressed as a percentage of the bond’s face value. A higher coupon rate results in a higher coupon payment, and vice versa. The formula for calculating the coupon payment is: Coupon Payment = Face Value x Coupon Rate x Payment Frequency.

For example, consider a bond with a face value of $1,000 and a coupon rate of 5%. The annual coupon payment would be $50 (1,000 x 0.05). If the bond pays coupons semi-annually, the semi-annual coupon payment would be $25 (1,000 x 0.05 / 2).

Understanding the relationship between coupon rate and coupon payment is essential for investors and analysts. It enables them to assess the potential returns and risks associated with a particular bond. Bonds with higher coupon rates tend to be more attractive to investors seeking regular income, while bonds with lower coupon rates may offer potential for capital appreciation.

Payment Frequency

In the context of how to calculate coupon payment, payment frequency holds significant importance. It refers to the number of times per year that coupon payments are made to bondholders. The payment frequency directly affects the calculation of coupon payment amounts.

For instance, bonds with semi-annual payment frequency will have their coupon payments calculated and distributed every six months. In contrast, bonds with annual payment frequency will have their coupon payments calculated and distributed once a year. The formula for calculating coupon payment considers the payment frequency to determine the appropriate portion of the annual coupon to be paid during each payment period.

Understanding payment frequency is crucial for investors and analysts as it influences the timing and amount of coupon payments received. This understanding aids in assessing the cash flow patterns associated with bond investments and enables informed decision-making regarding investment strategies.

Accrual Period

Within the framework of how to calculate coupon payment, understanding the concept of the accrual period is essential for accurate and timely calculation. The accrual period refers to the duration over which interest on a bond accrues and accumulates before it is paid out as a coupon payment to bondholders.

The accrual period plays a pivotal role in determining the coupon payment amount. It serves as the basis for calculating the portion of interest earned during a specific period. This calculation is crucial because it ensures that bondholders receive a fair and proportionate share of the total interest due on the bond. Without considering the accrual period, the calculation of coupon payments would be inaccurate and could lead to incorrect interest payments to bondholders.

In practice, the accrual period is typically aligned with the payment frequency of the bond. For instance, if a bond has semi-annual coupon payments, the accrual period would be six months. This alignment ensures that the coupon payment represents the interest earned over the preceding six-month period. Understanding the accrual period is also essential for investors and analysts when evaluating and comparing bonds. It allows for proper assessment of the timing and frequency of coupon payments, which can influence investment decisions and portfolio management strategies.

In conclusion, the accrual period holds significant importance in the calculation of coupon payments. It serves as the foundation for determining the portion of interest earned during a specific period and ensuring accurate and timely coupon payments to bondholders. Understanding the accrual period empowers investors and analysts to make informed investment decisions and effectively manage their bond portfolios.

Ex-Dividend Date

The ex-dividend date, a crucial concept intertwined with coupon payment calculations, signifies the cut-off point for dividend or coupon payment eligibility to investors. Those acquiring the bond or stock after this date are not entitled to the upcoming dividend or coupon payment. Understanding the ex-dividend date is pivotal in accurately determining coupon payments.

To illustrate, consider a bond with a semi-annual coupon payment schedule and an ex-dividend date of May 15th. Investors purchasing this bond on or after May 15th will not receive the forthcoming coupon payment, which is typically paid on a subsequent date, such as June 1st. The rationale behind this is to ensure that the seller, who held the bond up until the ex-dividend date, receives the coupon payment, as it represents the interest accrued during their ownership period.

For investors, being cognizant of the ex-dividend date is essential. Purchasing a bond just before the ex-dividend date allows for the receipt of the upcoming coupon payment, effectively increasing the yield on the investment. Conversely, purchasing a bond on or after the ex-dividend date means foregoing the upcoming coupon payment, which can impact the overall return on investment.

In conclusion, the ex-dividend date serves as a demarcation line for coupon payment eligibility. It is a critical component of how to calculate coupon payment and can influence investment decisions. By understanding the ex-dividend date, investors can optimize their bond purchases and maximize their returns.

Payment Date

Payment date, an integral aspect of how to calculate coupon payment, signifies the specific day on which coupon payments are distributed to bondholders. Understanding the payment date’s significance is crucial for accurate coupon payment calculations and effective bond portfolio management.

The payment date is directly tied to the bond’s coupon payment schedule, which outlines the frequency and timing of coupon payments. For instance, a bond with semi-annual coupon payments may have payment dates set on June 15th and December 15th each year. The payment date serves as a benchmark for calculating the accrual period, which determines the portion of interest earned since the last coupon payment.

Accurately calculating the payment date is essential to avoid errors in determining the accrued interest and ensuring timely receipt of coupon payments. Investors and analysts rely on accurate payment date information to make informed investment decisions, assess cash flows, and manage their bond portfolios efficiently.

In summary, understanding the relationship between payment date and how to calculate coupon payment is crucial for various stakeholders in the bond market. It enables accurate coupon payment calculations, effective portfolio management, and informed investment decisions. By considering the payment date alongside other factors such as the coupon rate, face value, and accrual period, investors and analysts can maximize the benefits and mitigate the risks associated with bond investments.

Clean Price

In the context of how to calculate coupon payment, understanding the concept of clean price is essential. Clean price, also known as accrued interest price, refers to the price of a bond that excludes any accrued but unpaid interest. It is a crucial component in accurately calculating coupon payments and determining the true value of a bond.

The relationship between clean price and how to calculate coupon payment is closely intertwined. The clean price is used as the basis for calculating the accrued interest, which represents the portion of interest that has accumulated since the last coupon payment date. Accrued interest is added to the clean price to arrive at the dirty price, which is the total price of the bond that includes both the principal and accrued interest.

Real-life examples showcase the practical applications of clean price in how to calculate coupon payment. Consider a bond with a face value of $1,000, a coupon rate of 5%, and a semi-annual coupon payment schedule. One month after the last coupon payment date, the bond’s clean price may be $995, reflecting the accrued interest that has accumulated over the past month. To calculate the coupon payment, the accrued interest would be added to the clean price, resulting in a dirty price of $1,000, which represents the total amount to be paid on the coupon payment date.

Understanding the relationship between clean price and how to calculate coupon payment is crucial for various stakeholders in the bond market. It enables accurate pricing of bonds, calculation of accrued interest, and effective portfolio management. By considering the clean price alongside other factors such as the coupon rate, face value, and payment date, investors and analysts can maximize the benefits and mitigate the risks associated with bond investments.

Dirty Price

Dirty price, an integral aspect of how to calculate coupon payment, incorporates the accrued interest along with the clean price (bond price excluding accrued interest) to determine the total bond price. This plays a significant role in accurate coupon payment calculations, as well as effective financial decision-making.

- Components: The dirty price comprises the clean price, which is the bond price without accrued interest, and the accrued interest, which is the interest that has accumulated since the last coupon payment date.

- Real-life Example: Consider a bond with a face value of $1,000, a coupon rate of 5%, and a semi-annual coupon payment schedule. One month after the last coupon payment date, the bond’s clean price may be $995, while its dirty price would typically be $1,000, reflecting the inclusion of accrued interest.

- Significance in Coupon Payment Calculation: To calculate the coupon payment, the accrued interest is added to the clean price, resulting in the dirty price. This is because the coupon payment represents the interest due to the bondholder, which includes both the accrued interest and the portion of interest that has been earned since the last coupon payment.

- Implications for Investors: Understanding dirty price is crucial for investors as it influences the overall yield and return on investment. Bonds trading at a premium (dirty price higher than face value) offer a lower yield compared to bonds trading at a discount (dirty price lower than face value).

In essence, dirty price provides a comprehensive view of a bond’s value by incorporating both the principal and accrued interest. It serves as a vital factor in calculating coupon payments, assessing bond yields, and making informed investment decisions in the bond market.

{FAQs on How to Calculate Coupon Payment}

This section addresses frequently asked questions (FAQs) related to calculating coupon payments on bonds, providing clear and concise answers to common concerns and misconceptions.

Question 1: What is the formula for calculating coupon payments?

Answer: Coupon Payment = Face Value x Coupon Rate x Payment Frequency

Question 2: How does the payment frequency affect coupon payments?

Answer: Payment frequency determines how often coupon payments are made, which influences the calculation of coupon payment amounts.

Question 3: What is the significance of the accrual period in coupon payment calculations?

Answer: The accrual period determines the portion of interest earned during a specific period, which is essential for accurate coupon payment calculations.

Question 4: What is the ex-dividend date, and how does it relate to coupon payments?

Answer: The ex-dividend date is the cut-off point for dividend or coupon payment eligibility. Investors purchasing a bond on or after this date will not receive the upcoming coupon payment.

Question 5: How is the clean price used in coupon payment calculations?

Answer: The clean price, excluding accrued interest, is used as the basis for calculating accrued interest, which is then added to the clean price to arrive at the dirty price for coupon payment calculations.

Question 6: What is the difference between clean price and dirty price?

Answer: The clean price excludes accrued interest, while the dirty price includes both the clean price and accrued interest. The dirty price represents the total bond price.

These FAQs provide fundamental insights into calculating coupon payments, addressing key aspects and potential areas of confusion. Understanding these concepts is crucial for accurate bond valuation, investment decision-making, and effective bond portfolio management.

In the following section, we will delve deeper into advanced considerations and strategies related to coupon payment calculations, including factors influencing coupon payment variability and methods for assessing bond value based on coupon payments.

Tips for Calculating Coupon Payments

This section offers practical tips to enhance the accuracy and efficiency of your coupon payment calculations, ensuring a solid understanding of bond valuation and investment strategies.

Tip 1: Utilize a Coupon Payment Calculator: Leverage online or spreadsheet-based calculators specifically designed for coupon payment calculations to minimize errors and save time.

Verify Bond Details: Before calculating coupon payments, meticulously review the bond’s prospectus or offering document to obtain accurate information regarding face value, coupon rate, and payment frequency.

Consider Accrual Periods: Accrual periods determine the portion of interest earned since the last coupon payment. Accurately identifying the accrual period is crucial for precise coupon payment calculations.

Pay Attention to Ex-Dividend Dates: The ex-dividend date signifies the cut-off point for coupon payment eligibility. Purchasing a bond on or after this date means you will not receive the upcoming coupon payment.

Differentiate Between Clean and Dirty Prices: Clean price represents the bond price excluding accrued interest, while dirty price includes both. Use the correct price based on your calculation needs.

Utilize Bond Pricing Formulas: Employ bond pricing formulas that incorporate coupon payments to assess the fair value of a bond and make informed investment decisions.

Incorporate Coupon Payments into Yield Calculations: Coupon payments are a key component of bond yields. Accurately incorporating them into yield calculations provides a comprehensive view of a bond’s return potential.

Consider Reinvestment Strategies: Explore strategies for reinvesting coupon payments to potentially enhance overall returns. Consider factors such as interest rates and market conditions.

By following these practical tips, you can refine your coupon payment calculation skills, leading to more precise bond valuations and informed investment decisions.

These tips lay the groundwork for the concluding section, where we will delve into strategies for managing and optimizing coupon payments to maximize bond portfolio performance.

Conclusion

This comprehensive exploration of coupon payment calculations has illuminated the intricate interplay of factors that influence bond valuation and investment strategies. Understanding the mechanics of coupon payment calculations empowers investors and analysts to make informed decisions, effectively manage bond portfolios, and navigate the complexities of the bond market.

Key takeaways from this analysis include:

- Accurately calculating coupon payments requires careful consideration of bond characteristics such as face value, coupon rate, payment frequency, and accrual periods.

- Utilizing financial tools and formulas, such as coupon payment calculators and bond pricing models, can enhance the precision and efficiency of coupon payment calculations.

- Incorporating coupon payments into yield calculations and reinvestment strategies provides a holistic view of a bond’s return potential and allows investors to optimize their investment portfolios.

As the bond market continues to evolve, staying abreast of the nuances of coupon payment calculations remains paramount. By mastering these concepts and leveraging available resources, investors can navigate the complexities of bond investments with confidence and achieve their financial goals.