Determining discount bond yield involves calculating the return on a bond that trades below its face value. For instance, a $1,000 bond available for $950 would have a discount yield.

Calculating discount bond yield is essential for investors seeking to evaluate potential returns on fixed-income securities. It provides insights into the bond’s market value and its relation to interest rates. Historically, discount bonds have played a significant role in capital markets, with their yields reflecting investor sentiment and economic conditions.

This article aims to provide a comprehensive guide to calculating discount bond yield, covering key formulas, practical applications, and implications for investment decisions.

How to Calculate Discount Bond Yield

Calculating discount bond yield is crucial for evaluating fixed-income investments. Key aspects include:

- Face value

- Purchase price

- Maturity date

- Coupon payments

- Yield to maturity

- Present value

- Accrued interest

- Holding period return

- Tax implications

- Market conditions

Understanding these aspects provides a comprehensive view of discount bond yield calculations. For instance, the face value and purchase price determine the bond’s discount, while the maturity date and coupon payments influence the yield to maturity. Market conditions and tax implications can also impact the overall return on the investment. By considering these factors, investors can make informed decisions when evaluating discount bonds.

Face Value

Face value is the nominal or par value of a bond, representing the amount to be repaid at maturity. It serves as a reference point for calculating discount bond yield and other key metrics.

- Nominal Amount: The face value represents the principal amount borrowed by the bond issuer, which is typically repaid in full at maturity.

- Bond Certificate: The face value is stated on the bond certificate and serves as a legal obligation for the issuer to repay the bondholder.

- Maturity Value: At maturity, the bondholder receives the face value, assuming no default or other complications.

- Discount Bonds: For discount bonds trading below face value, the difference between the face value and purchase price represents the discount.

Understanding face value is crucial for calculating discount bond yield, as it forms the basis for determining the bond’s present value and yield to maturity. Furthermore, face value plays a role in calculating accrued interest and holding period returns, providing investors with a comprehensive view of their bond investments.

Purchase price

Purchase price is a critical factor in calculating discount bond yield, as it determines the bond’s discount or premium. When a bond is purchased below its face value, it is considered a discount bond. Understanding the purchase price and its various facets is essential for accurate yield calculations.

- Par Value: The face value or nominal value of the bond, which is repaid at maturity.

- Market Price: The current price at which the bond is traded in the market, which may differ from the face value.

- Discount: The difference between the face value and the purchase price, which represents the amount below par that the bond is trading.

- Yield to Maturity (YTM): The internal rate of return (IRR) that equates the present value of the bond’s future cash flows to its purchase price.

These facets of purchase price are interconnected and influence the calculation of discount bond yield. The market price, which is influenced by supply and demand, determines the bond’s discount or premium. This discount, in turn, affects the yield to maturity, which is a key metric for evaluating the bond’s return potential. By considering these factors, investors can gain a deeper understanding of discount bond yield and make informed investment decisions.

Maturity date

Maturity date is a critical component of discount bond yield calculation. When a bond reaches maturity, the issuer must repay the bondholder the face value of the bond. Therefore, the time remaining until maturity significantly impacts the bond’s yield.

For example, a bond with a longer maturity date will have a higher yield to maturity than a bond with a shorter maturity date, assuming all other factors are equal. This is because investors require a higher return for tying up their money for a more extended period.

In calculating discount bond yield, the maturity date is used to determine the present value of the bond’s future cash flows. The present value is then used to calculate the yield to maturity, which is the annualized rate of return that the investor will receive if they hold the bond until maturity.

Understanding the relationship between maturity date and discount bond yield is essential for investors. By considering the time remaining until maturity, investors can make informed decisions about which bonds to purchase to meet their investment goals.

Coupon payments

Coupon payments play a crucial role in determining the yield of a discount bond. They represent periodic interest payments made by the bond issuer to the bondholder throughout the life of the bond, until its maturity date.

- Coupon rate: The fixed percentage of the face value of the bond that is paid as interest each year. This rate is set at the time of issuance and remains constant throughout the bond’s life.

- Coupon payment date: The specific date on which the coupon payment is made. Coupon payments are typically made semi-annually or annually.

- Accrued interest: The interest that has accumulated on the bond since the last coupon payment date. It is calculated as a prorated portion of the coupon payment and is added to the purchase price to determine the bond’s yield to maturity.

- Yield to maturity (YTM): The internal rate of return (IRR) that equates the present value of the bond’s future cash flows, including coupon payments and the face value at maturity, to its purchase price. The YTM is a key metric used to compare the yields of different bonds.

The calculation of discount bond yield takes into account the present value of all future coupon payments and the face value at maturity, discounted back to the present using the YTM. By considering the impact of coupon payments, investors can accurately assess the potential return on their investment in discount bonds.

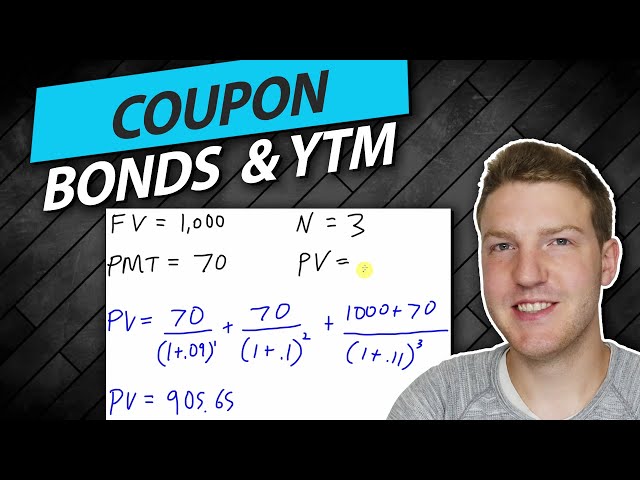

Yield to maturity

Yield to maturity (YTM) is a critical concept in calculating discount bond yield, representing the internal rate of return (IRR) that equates the present value of the bond’s future cash flows to its purchase price. Understanding YTM provides investors with valuable insights into the potential return on their investment.

- Coupon Payments: YTM considers the present value of all future coupon payments to be received until the bond’s maturity date. The coupon rate, payment frequency, and time to maturity all influence the calculation.

- Maturity Value: YTM also incorporates the present value of the bond’s face value or maturity value, which is repaid at the end of the bond’s life.

- Bond Price: The purchase price of the bond, which may be at a discount or premium to the face value, directly affects the YTM calculation. A higher bond price results in a lower YTM, and vice versa.

- Time to Maturity: The time remaining until the bond’s maturity date is a key factor in determining YTM. Generally, longer-term bonds have higher YTMs due to the increased uncertainty and risk associated with longer investment horizons.

By considering these facets of YTM, investors can gain a comprehensive understanding of how it relates to discount bond yield calculations. YTM provides a valuable metric for comparing the yields of different bonds and making informed investment decisions.

Present value

Present value (PV) plays a pivotal role in calculating the yield of a discount bond. It involves determining the current worth of future cash flows, discounted back to the present using an appropriate discount rate.

- Cash Flows: PV considers the present value of all future cash flows associated with the bond, including coupon payments and the face value at maturity.

- Discount Rate: The choice of discount rate, often the yield to maturity (YTM), is crucial in PV calculations as it reflects the time value of money.

- Time to Maturity: The time remaining until the bond’s maturity date is a key factor in determining PV, as it influences the discounting process.

- Compounding Effect: PV incorporates the effect of compounding, where interest earned on invested amounts is reinvested, leading to exponential growth over time.

Understanding these facets of present value is essential for accurate discount bond yield calculations. By considering the time value of money and the impact of compounding, investors can effectively assess the potential return on their investment.

Accrued Interest

Accrued interest represents the portion of interest that has accumulated on a bond since the last coupon payment date but has not yet been paid to the bondholder. It is a critical component in calculating the yield of a discount bond, as it directly impacts the bond’s present value and, consequently, its yield to maturity (YTM).

When a discount bond is purchased, the buyer pays the purchase price plus the accrued interest. This accrued interest is then added to the bond’s cost basis, which is used to calculate the bond’s yield to maturity. The YTM, in turn, reflects the annualized rate of return that the investor will receive if they hold the bond until maturity, taking into account the present value of all future cash flows, including coupon payments and the face value at maturity.

In practice, accrued interest is calculated by multiplying the bond’s annual coupon rate by the number of days that have passed since the last coupon payment date, divided by the number of days in the coupon period. This value is then added to the bond’s purchase price to determine the total cost of the investment. By accurately incorporating accrued interest into the yield calculation, investors can gain a more precise understanding of the bond’s potential return.

Understanding the connection between accrued interest and discount bond yield is essential for investors seeking to evaluate and compare different fixed-income investments. By considering the impact of accrued interest on the bond’s cost basis and yield to maturity, investors can make informed decisions that align with their investment goals and risk tolerance.

Holding Period Return

In the context of calculating discount bond yield, holding period return represents the total return an investor can expect to earn over the period they hold the bond. It encompasses components such as coupon payments, capital appreciation, and potential price changes, providing a comprehensive measure of the investment’s performance.

- Coupon Payments: Regular interest payments made by the bond issuer, providing a steady stream of income for the investor.

- Capital Appreciation: The potential increase in the bond’s market value over time, influenced by factors such as changes in interest rates and market demand.

- Price Changes: Fluctuations in the bond’s market price due to supply and demand dynamics, affecting the investor’s overall return.

- Accrued Interest: Interest earned since the last coupon payment date, added to the bond’s purchase price to determine the total investment cost and yield.

By considering these facets of holding period return, investors can gain insights into the potential return and risk associated with discount bond investments. Analyzing the historical performance of similar bonds, evaluating market conditions, and assessing the issuer’s financial health can further enhance investors’ decision-making process and help them make informed choices that align with their investment objectives.

Tax implications

Tax implications play a crucial role in calculating discount bond yield, as they affect the after-tax return an investor receives on their investment. These implications stem from the treatment of bond-related income and expenses under various tax jurisdictions.

- Tax on Coupon Payments: Interest income earned from bond coupons is generally subject to taxation as ordinary income, depending on the investor’s tax bracket and applicable tax laws.

- Tax on Discount at Purchase: If a discount bond is purchased below its face value, the difference (discount) is typically recognized as taxable income over the life of the bond, known as “bond premium amortization.”

- Tax on Capital Gains/Losses: When a discount bond is sold, any capital gain or loss realized is subject to capital gains or losses tax rates, depending on the holding period and the tax jurisdiction.

- Tax-Exempt Bonds: Certain bonds, such as municipal bonds, may offer tax-exempt status, meaning the interest income earned is not subject to federal or state income taxes, providing potential tax savings for investors.

Understanding these tax implications and incorporating them into discount bond yield calculations is essential for investors to assess the after-tax return on their investment and make informed investment decisions. Tax laws and regulations can vary depending on the jurisdiction, so it is advisable to consult with a tax professional or refer to relevant tax resources for specific guidance.

Market conditions

Market conditions play a significant role in determining the yield of a discount bond. The interplay between supply and demand, economic growth, and interest rate movements can influence the price of the bond, which ultimately impacts its yield calculation. When market conditions are favorable, with high demand for bonds and low interest rates, discount bonds tend to trade closer to their face value, resulting in a lower yield.

Conversely, in unfavorable market conditions, characterized by reduced demand and rising interest rates, discount bonds may trade at a deeper discount to their face value, leading to a higher yield. This relationship highlights the importance of considering market conditions when calculating discount bond yield, as they can significantly affect the potential return on investment.

For instance, during periods of economic uncertainty, investors may flock to safe-haven assets like government bonds, driving up their prices and reducing their yields. In contrast, during periods of economic growth and rising inflation, investors may seek higher returns, leading to increased demand for riskier assets and potentially higher yields on discount bonds.Understanding the impact of market conditions on discount bond yield is crucial for investors to make informed decisions and adjust their investment strategies accordingly.

Frequently Asked Questions on Calculating Discount Bond Yield

This section addresses common queries and clarifies aspects related to calculating discount bond yield, providing valuable insights to enhance understanding.

Question 1: What is the formula for calculating discount bond yield?

Answer: Discount bond yield is calculated using the following formula: Yield = (Face Value – Purchase Price) / ((Face Value + Purchase Price) / 2) * (360 / Days to Maturity)

Question 2: How does the purchase price of a discount bond impact its yield?

Answer: A lower purchase price relative to the face value results in a higher discount bond yield, as it represents a greater discount.

Question 3: What is the relationship between maturity date and discount bond yield?

Answer: Longer maturities generally lead to higher discount bond yields, as investors demand a higher return for committing their funds for a more extended period.

Question 4: How are coupon payments considered in discount bond yield calculations?

Answer: Coupon payments are added to the face value when calculating the present value of future cash flows, which is used to determine the discount bond yield.

Question 5: What role do market conditions play in discount bond yield?

Answer: Favorable market conditions, such as high demand and low interest rates, can lead to lower discount bond yields, while unfavorable conditions can result in higher yields.

Question 6: How does tax treatment affect discount bond yield calculations?

Answer: Tax implications, such as the treatment of coupon payments and discount amortization, can influence the after-tax return and should be considered when calculating discount bond yield.

These FAQs provide a concise overview of key considerations and potential queries related to calculating discount bond yield, equipping investors with a solid foundation for further exploration.

In the next section, we will delve into advanced strategies and practical applications of discount bond yield calculations to enhance investment decision-making.

Tips for Calculating Discount Bond Yield

This section provides concrete tips to enhance the accuracy and effectiveness of discount bond yield calculations, empowering investors with practical guidance for sound investment decisions.

Tip 1: Utilize Bond Pricing Calculators: Employ online bond pricing calculators or spreadsheet functions to simplify and streamline yield calculations, ensuring precision and saving time.

Tip 2: Consider Accrued Interest: Remember to incorporate accrued interest into the bond’s purchase price, as it represents earned but unpaid interest, affecting the yield calculation.

Tip 3: Understand Time Value of Money: Recognize the impact of time on the value of money, as future cash flows are discounted back to the present to determine the yield.

Tip 4: Assess Market Conditions: Stay informed about current market conditions, as they influence bond prices and, consequently, discount bond yields.

Tip 5: Evaluate Issuer Creditworthiness: Consider the creditworthiness of the bond issuer, as it affects the risk premium and, in turn, the yield.

Tip 6: Compare Yields: Compare the yields of different discount bonds to identify potential opportunities and make informed investment choices.

By following these tips, investors can enhance their understanding of discount bond yield calculations and make more informed investment decisions, maximizing the potential return on their fixed-income investments.

The subsequent section will delve into advanced strategies for utilizing discount bond yield calculations to optimize investment portfolios and achieve long-term financial goals.

Conclusion

This comprehensive exploration of “How to Calculate Discount Bond Yield” has illuminated the intricacies and significance of this calculation in the realm of fixed-income investments. Understanding the factors that influence discount bond yield, such as purchase price, maturity date, coupon payments, market conditions, and tax implications, empowers investors to make informed decisions.

Key takeaways include the inverse relationship between purchase price and yield, the positive correlation between maturity and yield, and the impact of market conditions on bond pricing and yield. Additionally, the incorporation of accrued interest and consideration of issuer creditworthiness are crucial for accurate calculations.

By mastering these concepts, investors can harness the potential of discount bond yield calculations to optimize their investment portfolios and achieve long-term financial goals. This knowledge empowers them to navigate the complexities of the bond market and make sound investment decisions that align with their risk tolerance and return expectations.