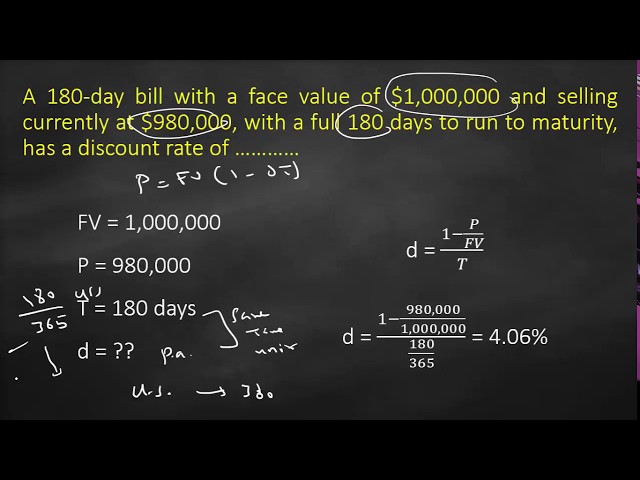

The discount rate formula is a critical tool used in finance to determine the present value of future cash flows. It is calculated by adjusting a nominal interest rate for the expected rate of inflation.

The formula is relevant because it allows investors and businesses to make informed decisions about investments, capital budgeting, and financial planning. It is also essential in evaluating the viability of projects and determining the appropriate cost of capital. Historically, the concept of discounting cash flows has been attributed to the mathematician and astronomer Edmund Halley in the 17th century.

This article will delve into the details of the discount rate formula, explaining its components, variations, and applications. By understanding the principles behind this formula, readers can gain valuable insights into financial decision-making and investment strategies.

How to Calculate Discount Rate Formula

The discount rate formula is a critical tool in finance, used to calculate the present value of future cash flows. It is essential for evaluating investments, capital budgeting, and financial planning. Understanding the key aspects of the discount rate formula is crucial for accurate financial decision-making.

- Definition: The discount rate is the rate at which future cash flows are discounted to their present value.

- Formula: The discount rate formula is: Discount Rate = (1 + Nominal Interest Rate) / (1 + Inflation Rate) – 1

- Components: The discount rate formula consists of the nominal interest rate and the inflation rate.

- Variations: There are different variations of the discount rate formula, such as the real discount rate and the effective discount rate.

- Applications: The formula is used in various financial applications, including project evaluation, capital budgeting, and investment analysis.

- Importance: Using the correct discount rate is crucial for making sound financial decisions.

- Assumptions: The formula assumes that the nominal interest rate and inflation rate remain constant over the relevant period.

- Limitations: The formula does not account for all factors that may affect the value of future cash flows.

- Example: A project with an expected cash flow of $100,000 in one year, a nominal interest rate of 5%, and an inflation rate of 2% would have a discount rate of 2.94%.

These key aspects provide a comprehensive overview of the discount rate formula, highlighting its components, variations, applications, and limitations. By understanding these aspects, financial professionals and investors can effectively calculate the present value of future cash flows and make informed financial decisions.

Definition: The discount rate is the rate at which future cash flows are discounted to their present value.

This definition lies at the core of calculating the discount rate formula. The discount rate is the crucial element that transforms future cash flows into their present value equivalents. Without understanding this concept, it is impossible to accurately calculate the discount rate, which is essential for making informed financial decisions.

In real-life applications, the discount rate has numerous practical implications. For instance, in capital budgeting, the discount rate aids in evaluating the profitability of long-term projects. It helps businesses determine whether potential investments align with their financial goals and risk tolerance. Moreover, the discount rate plays a significant role in valuing bonds and other fixed-income securities, enabling investors to assess their worth and make informed investment choices.

By understanding the connection between the definition of the discount rate and the formula used to calculate it, financial professionals and investors gain valuable insights. They can make sound judgments about the present value of future cash flows, compare investment opportunities, and optimize their financial strategies. This understanding empowers them to make well-informed decisions that align with their financial objectives, contributing to long-term financial success.

Formula: The discount rate formula is: Discount Rate = (1 + Nominal Interest Rate) / (1 + Inflation Rate) – 1

Within the framework of “how to calculate discount rate formula,” this formula serves as the cornerstone for determining the discount rate. It establishes the relationship between the nominal interest rate, inflation rate, and the resulting discount rate, which is crucial for accurately evaluating future cash flows.

- Nominal Interest Rate: The nominal interest rate represents the stated or face value of the interest rate, not adjusted for inflation. In the formula, it signifies the expected nominal return on an investment.

- Inflation Rate: The inflation rate measures the percentage change in the general price level of goods and services over time. It captures the impact of inflation on the value of future cash flows.

- Discount Rate: The discount rate is the rate used to discount future cash flows to their present value. It reflects the time value of money and the opportunity cost of capital.

- Relationship: The formula establishes an inverse relationship between the discount rate and the nominal interest rate and inflation rate. A higher nominal interest rate or inflation rate will result in a higher discount rate, leading to a lower present value of future cash flows.

By understanding the individual components of this formula and their interrelationships, financial professionals can accurately calculate the discount rate, a fundamental component of various financial analyses. This understanding empowers informed decision-making and enables sound financial planning for individuals and organizations alike.

Components: The discount rate formula consists of the nominal interest rate and the inflation rate.

Within the framework of “how to calculate discount rate formula,” understanding the components of the formula is crucial. The nominal interest rate and inflation rate are the two essential elements that determine the discount rate.

The nominal interest rate represents the stated return on an investment, while the inflation rate measures the change in the general price level over time. The relationship between these components and the discount rate formula is inverse. A higher nominal interest rate or inflation rate will result in a higher discount rate, which in turn reduces the present value of future cash flows.

For instance, consider an investment with an expected cash flow of $10,000 in one year. If the nominal interest rate is 5% and the inflation rate is 2%, the discount rate would be approximately 2.94%. This means that the present value of the $10,000 cash flow would be approximately $9,712.20.

Understanding the relationship between the components of the discount rate formula and the impact on the present value of future cash flows is critical for financial decision-making. It enables investors and businesses to accurately assess the value of long-term investments and make informed choices about capital allocation.

Variations: There are different variations of the discount rate formula, such as the real discount rate and the effective discount rate.

Within the framework of “how to calculate discount rate formula,” understanding the different variations is critical. The real discount rate and the effective discount rate are two significant variations that serve specific purposes.

The real discount rate is the nominal discount rate adjusted for inflation. It represents the actual return on an investment in real terms, taking into account the impact of inflation on the purchasing power of money. The effective discount rate, on the other hand, considers the compounding effect of interest over multiple periods. It provides a more accurate representation of the true cost of borrowing or the true return on an investment when interest is compounded frequently.

The choice of discount rate variation depends on the specific context and the purpose of the analysis. In situations where inflation is a significant factor, the real discount rate is more appropriate as it provides a more accurate assessment of the time value of money. Conversely, the effective discount rate is more suitable when interest is compounded frequently, ensuring a more precise calculation of the investment’s true cost or return.

Understanding the different variations of the discount rate formula and their implications is crucial for accurate financial analysis. By selecting the appropriate variation based on the specific context, financial professionals and investors can make informed decisions, assess the viability of investments, and optimize their financial strategies.

Applications: The formula is used in various financial applications, including project evaluation, capital budgeting, and investment analysis.

The discount rate formula finds applications across a wide range of financial decision-making processes, serving as a cornerstone for evaluating the viability and profitability of investments and projects.

- Project Evaluation:

The discount rate is crucial in assessing the profitability of long-term projects. It helps businesses determine whether potential investments align with their financial goals and risk tolerance. By discounting future cash flows to their present value, companies can make informed decisions about capital allocation and project selection.

- Capital Budgeting:

Capital budgeting involves making investment decisions that impact the long-term growth and financial health of a company. The discount rate plays a central role in this process, enabling businesses to compare and select projects based on their net present value. It ensures that investment decisions are aligned with the organization’s overall financial objectives.

- Investment Analysis:

The discount rate is fundamental in investment analysis, particularly in valuing fixed-income securities such as bonds. By discounting future coupon payments and the principal repayment to their present value, investors can assess the fair value of bonds and make informed decisions about their investment portfolios.

- Cost of Capital:

The discount rate also serves as a proxy for the cost of capital, representing the minimum required return that investors expect for providing financing. This concept is crucial for businesses seeking external financing, as it influences the cost of borrowing and impacts overall financial planning.

These applications underscore the versatility and importance of the discount rate formula in financial decision-making. By understanding the principles behind this formula and its various applications, financial professionals and investors can make informed choices, optimize their financial strategies, and achieve long-term financial success.

Importance: Using the correct discount rate is crucial for making sound financial decisions.

The importance of using the correct discount rate stems from its direct impact on financial decision-making, particularly in capital budgeting and investment analysis. The discount rate serves as a critical component of the calculation process, as it determines the present value of future cash flows, which is essential for evaluating the viability and profitability of investments.

Real-life examples abound where the correct discount rate has played a pivotal role in making sound financial decisions. Consider a company faced with two investment projects, each with varying cash flow patterns. By using an appropriate discount rate, the company can accurately compare the present value of each project’s future cash flows, enabling it to select the investment with the higher potential return and lower risk.

The practical applications of this understanding extend beyond project evaluation. In investment analysis, for instance, the correct discount rate helps investors determine the fair value of bonds and other fixed-income securities. This knowledge empowers them to make informed investment decisions, optimize their portfolios, and achieve long-term financial goals.

In summary, the discount rate formula is a powerful tool for financial decision-making, and using the correct discount rate is paramount for making sound financial decisions. By understanding the connection between the discount rate formula and its applications, financial professionals and investors can gain invaluable insights into the time value of money and make informed choices that drive financial success.

Assumptions: The formula assumes that the nominal interest rate and inflation rate remain constant over the relevant period.

In the context of the discount rate formula, this assumption plays a crucial role in determining the present value of future cash flows and, consequently, shaping financial decision-making. The formula relies on the assumption that both the nominal interest rate and inflation rate will remain constant throughout the relevant period, which may not always hold true in real-world scenarios.

- Constancy of Nominal Interest Rate:

The formula assumes that the nominal interest rate will remain unchanged over the relevant period. This assumption simplifies the calculation process but may not reflect the dynamic nature of interest rates in practice. Fluctuations in interest rates can significantly impact the present value of future cash flows, particularly for long-term investments or projects.

- Constancy of Inflation Rate:

The formula also assumes that the inflation rate will remain constant over the relevant period. This assumption allows for a straightforward calculation of the real discount rate and the present value of future cash flows. However, inflation rates are often subject to change due to economic factors, government policies, or global events. Variations in inflation can alter the purchasing power of money and affect the real value of future cash flows.

- Impact on Decision-Making:

The assumption of constant interest and inflation rates can have implications for financial decision-making. If these rates change significantly during the relevant period, the present value of future cash flows calculated using the discount rate formula may not accurately reflect their true value. This can lead to suboptimal investment decisions or project evaluations.

Despite its limitations, the discount rate formula remains a valuable tool for financial analysis. By understanding the assumptions behind the formula and their potential impact on decision-making, financial professionals and investors can make informed judgments and incorporate appropriate risk assessments into their strategies.

Limitations: The formula does not account for all factors that may affect the value of future cash flows.

Within the framework of “how to calculate discount rate formula,” understanding the limitations of the formula is crucial for making informed financial decisions. The formula assumes constant interest rates and inflation rates, which may not always hold true in practice. Additionally, there are other factors that can influence the value of future cash flows that are not captured by the formula.

- Uncertain Economic Conditions:

The formula does not consider potential changes in economic conditions, such as recessions or booms, which can significantly impact future cash flows.

- Technological Advancements:

The formula does not account for the potential impact of technological advancements, which can disrupt industries and alter the value of future cash flows.

- Political or Regulatory Changes:

The formula does not incorporate the potential effects of political or regulatory changes, which can influence the business environment and the value of future cash flows.

- Company-Specific Factors:

The formula does not consider company-specific factors, such as changes in management, competition, or market share, which can affect the value of future cash flows.

These limitations highlight the need for careful consideration when using the discount rate formula. Financial professionals and investors should be aware of these limitations and incorporate appropriate risk assessments into their decision-making processes. By understanding the potential factors that can affect the value of future cash flows, they can make more informed judgments and improve the accuracy of their financial projections.

Example: A project with an expected cash flow of $100,000 in one year, a nominal interest rate of 5%, and an inflation rate of 2% would have a discount rate of 2.94%.

This example serves as a practical illustration of the discount rate formula and its application in financial decision-making. By examining its components and implications, we gain a deeper understanding of how the discount rate is calculated and used.

- Discount Rate Formula:

The example showcases the application of the discount rate formula: Discount Rate = (1 + Nominal Interest Rate) / (1 + Inflation Rate) – 1. Using the given values, we arrive at a discount rate of 2.94%.

- Time Value of Money:

This example highlights the concept of the time value of money. The discount rate adjusts future cash flows to their present value, recognizing that money today is worth more than the same amount in the future due to its earning potential.

- Inflation Adjustment:

The example demonstrates the importance of adjusting for inflation when calculating the discount rate. The inflation rate is incorporated into the formula to ensure that the discount rate accurately reflects the expected decrease in the purchasing power of money over time.

- Financial Decision-Making:

This example underscores the significance of the discount rate in financial decision-making. The calculated discount rate of 2.94% becomes a crucial input for evaluating the project’s profitability and making informed investment choices.

By delving into the specifics of this example, we have gained valuable insights into the components, implications, and applications of the discount rate formula. These insights equip financial professionals and investors with the knowledge necessary to make sound financial decisions and achieve their investment goals.

Frequently Asked Questions on Discount Rate Formula Calculations

This section addresses common queries and misconceptions surrounding the calculation of discount rate formulas. These FAQs aim to clarify key aspects and provide additional insights for financial professionals and investors.

Question 1: What is the significance of the nominal interest rate in the discount rate formula?

Answer: The nominal interest rate represents the stated or face value of the interest rate, not adjusted for inflation. It reflects the expected nominal return on an investment. A higher nominal interest rate results in a higher discount rate, leading to a lower present value of future cash flows.

Question 2: How does inflation affect the discount rate calculation?

Answer: Inflation reduces the purchasing power of money over time. By incorporating the inflation rate into the discount rate formula, we adjust for the expected decrease in the value of money, resulting in a more accurate calculation of the present value of future cash flows.

Question 3: What are the limitations of the discount rate formula?

Answer: While the discount rate formula provides a useful framework for evaluating future cash flows, it doesn’t account for all factors that may affect their value. Uncertain economic conditions, technological advancements, political changes, and company-specific factors can influence the accuracy of the calculated discount rate.

Question 4: How do I choose the appropriate discount rate for my financial analysis?

Answer: The appropriate discount rate depends on the specific context and purpose of the analysis. Factors to consider include the risk associated with the investment, the industry, and the company’s financial health. A higher risk typically warrants a higher discount rate.

Question 5: What is the relationship between the discount rate and the net present value (NPV) of an investment?

Answer: The discount rate is used to calculate the NPV of an investment. A higher discount rate results in a lower NPV, indicating a lower present value of future cash flows and potentially a less attractive investment opportunity.

Question 6: How can I ensure the accuracy of my discount rate calculations?

Answer: To enhance the accuracy of your discount rate calculations, consider using reputable sources for interest rate and inflation data. Regularly review and update your discount rates to reflect changing economic conditions and market dynamics.

These FAQs provide valuable insights into the nuances of discount rate formula calculations. Understanding these aspects empowers financial professionals and investors to make informed decisions, conduct accurate financial analyses, and optimize their investment strategies.

In the next section, we will delve deeper into the applications of discount rate formulas, exploring their usage in project evaluation, capital budgeting, and investment analysis.

Tips for Discount Rate Formula Calculations

To enhance the accuracy and effectiveness of your discount rate formula calculations, consider implementing the following practical tips:

Tip 1: Utilize Reputable Data Sources: Obtain interest rate and inflation data from reliable and up-to-date sources to ensure the accuracy of your calculations.

Tip 2: Regularly Review and Update: Periodically review and adjust your discount rates to reflect changing economic conditions and market dynamics.

Tip 3: Consider Risk Factors: When selecting a discount rate, take into account the level of risk associated with the investment or project being evaluated. Higher risk typically warrants a higher discount rate.

Tip 4: Incorporate Company-Specific Factors: For project-level evaluations, consider incorporating company-specific factors that may influence future cash flows, such as changes in management or market share.

Tip 5: Use a Range of Discount Rates: To account for uncertainty, consider using a range of discount rates rather than a single rate. This provides a more comprehensive analysis of potential outcomes.

Tip 6: Seek Professional Advice: If required, consult with a financial professional or expert to ensure the appropriate use and interpretation of discount rate formulas.

Summary: By following these tips, you can enhance the accuracy and reliability of your discount rate calculations, leading to more informed financial decisions and improved investment outcomes.

In the concluding section, we will explore advanced applications of discount rate formulas, including their use in complex financial modeling and risk analysis.

Conclusion

This comprehensive guide has provided an in-depth exploration of the discount rate formula, its components, and its diverse applications in financial analysis. Key insights include the formula’s dependence on nominal interest rate and inflation rate, the need to account for risk and uncertainty, and the importance of using reliable data sources.

To summarize, the discount rate formula serves as a vital tool for evaluating the time value of money and making informed financial decisions. Its versatility extends from project appraisal and capital budgeting to investment analysis and risk assessment. By understanding the intricacies of this formula, financial professionals can effectively navigate the complex landscape of financial markets.