Discount rate is the interest rate used to convert future cash flows into a present value.

Determining the discount rate is a crucial step in capital budgeting and investment analysis.

This article will provide a step-by-step guide on how to calculate the discount rate using a BA II Plus calculator.

How to Calculate Discount Rate on BA II Plus

Determining the discount rate is a crucial step in capital budgeting and investment analysis. The discount rate is the interest rate used to convert future cash flows into a present value, and there are several key aspects to consider when calculating the discount rate using a BA II Plus calculator.

- Time value of money

- Risk-free rate

- Project risk

- Inflation

- Calculator functions

- Formula inputs

- Accuracy and precision

- Interpretation of results

- Applications in finance

These aspects are all interconnected and play a vital role in the accurate calculation of the discount rate. Understanding the concepts behind each of these aspects will help ensure that the discount rate is calculated correctly and that the resulting investment decisions are sound.

Time Value of Money

The concept of time value of money (TVM) is fundamental to understanding how to calculate the discount rate on a BA II Plus calculator. TVM recognizes that the value of money changes over time due to the effects of inflation and interest rates. A dollar today is worth more than a dollar in the future because it has the potential to earn interest. Conversely, a dollar in the future is worth less than a dollar today because of the erosive effects of inflation.

When calculating the discount rate, it is important to consider the time value of money to ensure that future cash flows are appropriately discounted to their present value. The discount rate is the rate at which future cash flows are discounted, and it should reflect the rate at which money can be invested and earn a return. If the discount rate is too low, then future cash flows will be overvalued, and the investment may appear more attractive than it actually is. Conversely, if the discount rate is too high, then future cash flows will be undervalued, and the investment may appear less attractive than it actually is.

In practice, the time value of money is used in a variety of financial applications, including capital budgeting, investment analysis, and loan pricing. By understanding the time value of money and how it impacts the calculation of the discount rate, financial professionals can make more informed investment decisions.

Risk-free rate

The risk-free rate is a critical component of the discount rate calculation. It is the rate of return that investors can expect to earn on a risk-free investment, such as a government bond. The risk-free rate is used as the base rate for calculating the discount rate, and it represents the minimum rate of return that investors require to compensate them for the time value of money.

The risk-free rate is important because it affects the cost of capital for businesses. A higher risk-free rate will lead to a higher discount rate, which will make it more expensive for businesses to borrow money. Conversely, a lower risk-free rate will lead to a lower discount rate, which will make it cheaper for businesses to borrow money.

In practice, the risk-free rate is used by businesses to calculate the cost of capital for their projects. The cost of capital is the minimum rate of return that a business must earn on a project in order to justify the investment. By using the risk-free rate as the base rate, businesses can calculate the cost of capital and make informed investment decisions.

Here is an example of how the risk-free rate is used to calculate the discount rate:“`Discount rate = Risk-free rate + Risk premium“`where: Discount rate is the rate used to discount future cash flows Risk-free rate is the rate of return on a risk-free investment* Risk premium is the additional return required to compensate investors for the risk of the investment

By understanding the relationship between the risk-free rate and the discount rate, businesses can make more informed investment decisions and improve their financial performance.

Project risk

Project risk is a crucial factor to consider when calculating the discount rate on a BA II Plus calculator. It represents the uncertainty and potential variability associated with the project’s cash flows, and it can have a significant impact on the overall investment decision.

- Technical risk

Refers to the potential for delays, cost overruns, or other technical issues that could impact the project’s timeline or budget. Examples include unforeseen geological conditions, equipment failures, or regulatory changes.

- Market risk

Relates to the potential for changes in the market demand, competition, or economic conditions that could affect the project’s revenue or profitability. Examples include fluctuations in commodity prices, changes in consumer preferences, or shifts in the regulatory landscape.

- Financial risk

Involves the potential for financial distress or bankruptcy, which could impact the project’s ability to generate cash flows or repay debt. Examples include changes in interest rates, currency fluctuations, or unexpected tax liabilities.

- Operational risk

Refers to the potential for disruptions or inefficiencies in the project’s operations that could affect its costs or revenues. Examples include labor disputes, supply chain disruptions, or natural disasters.

Understanding and quantifying project risk is essential for calculating an appropriate discount rate. A higher level of project risk will typically lead to a higher discount rate, as investors will require a greater return to compensate for the increased uncertainty. Conversely, a lower level of project risk will typically lead to a lower discount rate, as investors will be more confident in the project’s cash flows. By incorporating project risk into the discount rate calculation, businesses can make more informed investment decisions and improve their overall risk management.

Inflation

Inflation is a crucial factor to consider when calculating the discount rate on a BA II Plus calculator. It represents the rate at which the general level of prices for goods and services is rising, and it can significantly impact the value of future cash flows.

- Purchasing power

Inflation erodes the purchasing power of money over time, meaning that each unit of currency can buy fewer goods and services in the future. This is a key consideration when calculating the discount rate, as future cash flows need to be adjusted for the effects of inflation to determine their present value accurately.

- Real interest rates

The discount rate is typically expressed in nominal terms, which means that it includes the effects of inflation. However, it is important to consider real interest rates when making investment decisions. Real interest rates are nominal interest rates minus the rate of inflation. By using real interest rates, investors can compare the actual return on their investments to the rate of inflation and make more informed decisions.

- Inflation expectations

Inflation expectations play a significant role in determining the discount rate. Investors will typically require a higher discount rate if they expect inflation to be high in the future. This is because they want to be compensated for the erosion of purchasing power that inflation will cause. Conversely, investors will be willing to accept a lower discount rate if they expect inflation to be low in the future.

- Central bank policy

Central banks play a significant role in managing inflation through monetary policy. By raising or lowering interest rates, central banks can influence the rate of inflation. This, in turn, can have a significant impact on the discount rate, as investors will adjust their expectations of future inflation based on the central bank’s actions.

In conclusion, inflation is a complex and multifaceted phenomenon that can significantly impact the calculation of the discount rate. By understanding the various facets of inflation and how they interact with the discount rate, investors can make more informed investment decisions and improve their overall financial performance.

Calculator functions

In the context of calculating the discount rate on a BA II Plus calculator, various calculator functions play crucial roles in facilitating accurate and efficient computations. These functions encompass a range of capabilities, from basic arithmetic operations to specialized financial calculations.

- Numeric keypad

The numeric keypad allows for the input of numerical values, including the discount rate, cash flows, and other relevant parameters. The accuracy of these inputs is paramount for obtaining reliable results.

- Financial functions

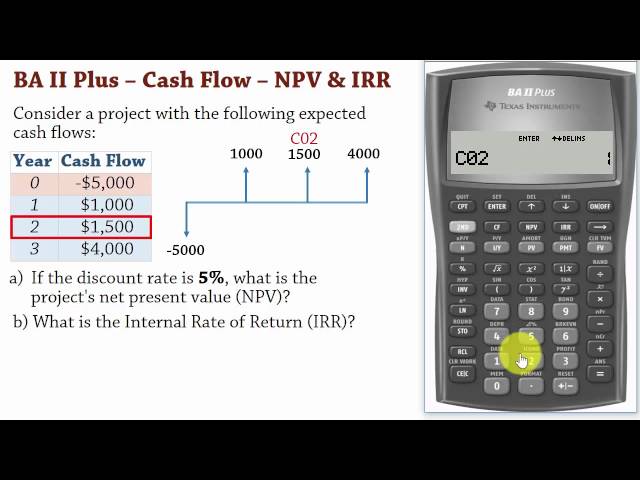

The BA II Plus calculator is equipped with a suite of financial functions specifically designed for calculating the discount rate and other financial metrics. These functions include the NPV (net present value) function, the IRR (internal rate of return) function, and the PMT (payment) function, among others.

- Statistical functions

Statistical functions can be utilized to analyze historical data and make informed assumptions about future cash flows. For example, the standard deviation function can be used to assess the variability of cash flows, which can influence the choice of discount rate.

- Memory and storage

The BA II Plus calculator features memory and storage capabilities, enabling users to save and recall intermediate results, as well as store frequently used values and formulas. This functionality enhances efficiency and reduces the risk of errors during complex calculations.

In summary, the calculator functions of the BA II Plus calculator provide a comprehensive set of tools for calculating the discount rate and performing other related financial computations. Familiarity with these functions empowers users to leverage the calculator’s capabilities effectively, ensuring accurate and reliable results in their financial analysis and investment decision-making.

Formula inputs

Formula inputs represent an integral aspect of calculating the discount rate using a BA II Plus calculator. These inputs serve as the foundation for the calculations and directly influence the accuracy and reliability of the resulting discount rate.

- Cash flows

Cash flows are the heart of any discount rate calculation. They represent the expected inflows and outflows of cash over the life of the project or investment. Accurately estimating and inputting cash flows is crucial, as any errors or omissions can significantly impact the calculated discount rate.

- Discount rate

The discount rate serves as the benchmark against which future cash flows are discounted to determine their present value. Selecting an appropriate discount rate is critical, as it reflects the time value of money and the risk associated with the project or investment.

- Time period

The time period over which the cash flows occur is another important input. It determines the number of periods for which the discount rate will be applied to discount future cash flows.

- Compounding frequency

Compounding frequency refers to the number of times per year that the discount rate is applied to the cash flows. This input affects the calculation of the present value and should be carefully considered based on the project’s or investment’s characteristics.

In summary, formula inputs play a pivotal role in calculating the discount rate on a BA II Plus calculator. Accurate and well-defined inputs are essential for obtaining reliable and meaningful results. By carefully considering the various facets of formula inputs, users can enhance the accuracy and precision of their discount rate calculations, leading to informed investment decisions.

Accuracy and precision

Accuracy and precision are two critical components of calculating the discount rate on a BA II Plus calculator. Accuracy refers to the closeness of the calculated discount rate to the true discount rate, while precision refers to the level of detail or number of decimal places in the calculated discount rate. Both accuracy and precision are important for making informed investment decisions.

In the context of calculating the discount rate, accuracy is important because it ensures that the calculated discount rate is a close approximation of the true discount rate. This is important because the discount rate is used to determine the present value of future cash flows, and an inaccurate discount rate can lead to incorrect investment decisions. Precision is also important because it allows for more precise calculations of the present value of future cash flows. This can be important for projects with long time horizons or for projects with small cash flows.

There are several factors that can affect the accuracy and precision of the calculated discount rate. These factors include the accuracy of the input data, the number of decimal places used in the calculation, and the rounding method used. It is important to be aware of these factors and to take steps to ensure that the calculated discount rate is accurate and precise.

In practice, accuracy and precision are essential for making informed investment decisions. By understanding the relationship between accuracy and precision and how they impact the calculation of the discount rate, investors can make more informed decisions and improve their overall investment performance.

Interpretation of results

The interpretation of results is a critical step in the process of calculating the discount rate on a BA II Plus calculator. After the discount rate has been calculated, it is important to interpret the results in order to make informed investment decisions. The interpretation of results involves understanding the meaning of the calculated discount rate and how it should be used in the decision-making process.

One important aspect of interpreting the results is to consider the accuracy and precision of the calculation. As discussed earlier, the accuracy and precision of the calculated discount rate can be affected by a number of factors. It is important to be aware of these factors and to take steps to ensure that the calculated discount rate is accurate and precise.

Another important aspect of interpreting the results is to consider the implications of the calculated discount rate for the investment decision. The discount rate is used to determine the present value of future cash flows, and the present value is used to make investment decisions. It is important to understand how the discount rate affects the present value and how this affects the investment decision.

In practice, the interpretation of results is an essential part of the process of calculating the discount rate on a BA II Plus calculator. By understanding the meaning of the calculated discount rate and how it should be used in the decision-making process, investors can make more informed investment decisions and improve their overall investment performance.

Applications in finance

The applications of the discount rate in finance are vast and far-reaching. It is a critical component of capital budgeting, investment analysis, and financial planning, and plays a vital role in determining the value of assets and liabilities.

In capital budgeting, the discount rate is used to evaluate the profitability of long-term investment projects. By discounting future cash flows back to the present day, businesses can determine the net present value (NPV) of a project, which is a measure of its profitability. The NPV is then used to make investment decisions, with projects that have a positive NPV typically being considered acceptable.

The discount rate is also used in investment analysis to evaluate the attractiveness of potential investments. By discounting future cash flows back to the present day, investors can determine the internal rate of return (IRR) of an investment, which is the rate of return that the investment is expected to generate. The IRR is then used to compare different investment opportunities and make investment decisions.

In financial planning, the discount rate is used to value assets and liabilities. By discounting future cash flows back to the present day, businesses can determine the present value of an asset or liability, which is a measure of its value. The present value is then used to make financial planning decisions, such as determining the amount of money that needs to be set aside for retirement or the value of a business.

The discount rate is a powerful tool that can be used to make a variety of financial decisions. By understanding the applications of the discount rate, financial professionals can make more informed decisions and improve their overall financial performance.

Frequently Asked Questions

This FAQ section provides answers to commonly asked questions and clarifies key concepts related to calculating the discount rate on a BA II Plus calculator.

Question 1: What is the discount rate?

Answer: The discount rate is the interest rate used to convert future cash flows into a present value. It represents the rate at which money can be invested and earn a return.

Question 2: How do I calculate the discount rate on a BA II Plus calculator?

Answer: To calculate the discount rate on a BA II Plus calculator, you can use the TVM (Time Value of Money) functions. These functions allow you to input the cash flows, number of periods, and compounding frequency to calculate the discount rate.

Question 3: What factors should I consider when choosing a discount rate?

Answer: When choosing a discount rate, you should consider factors such as the risk-free rate, project risk, inflation, and your investment objectives.

Question 4: How does the discount rate affect the present value of future cash flows?

Answer: The discount rate has an inverse relationship with the present value of future cash flows. A higher discount rate will result in a lower present value, and vice versa.

Question 5: What are some common applications of the discount rate in finance?

Answer: The discount rate is widely used in capital budgeting, investment analysis, and financial planning to evaluate the profitability of investments and value assets and liabilities.

Question 6: How can I improve the accuracy of my discount rate calculations?

Answer: To improve the accuracy of your discount rate calculations, ensure you have accurate input data and consider using a higher number of decimal places in your calculations.

These FAQs provide a concise overview of the key aspects of calculating the discount rate on a BA II Plus calculator. By understanding these concepts, you can effectively use this tool to make informed financial decisions.

In the next section, we will explore advanced techniques for calculating the discount rate and discuss the limitations and pitfalls to avoid.

Tips for Calculating Discount Rate on a BA II Plus Calculator

This section provides a comprehensive list of practical tips to enhance the accuracy, efficiency, and reliability of your discount rate calculations using a BA II Plus calculator.

Tip 1: Utilize the TVM Functions: Leverage the built-in Time Value of Money (TVM) functions specifically designed for discount rate calculations, such as NPV, IRR, and PMT.

Tip 2: Verify Input Accuracy: Meticulously review the accuracy of all input values, including cash flows, time periods, and compounding frequency, to ensure reliable results.

Tip 3: Consider Project Risk: Assess the level of uncertainty and potential risks associated with the project or investment to determine an appropriate discount rate that reflects the perceived risk.

Tip 4: Account for Inflation: Adjust for inflation by using real interest rates or incorporating an inflation premium into the discount rate calculation.

Tip 5: Use a Higher Precision: Employ a greater number of decimal places in your calculations to enhance the precision of the discount rate, especially for long-term projects or those with small cash flows.

Tip 6: Understand the Impact of Compounding: Recognize the effect of compounding frequency on the discount rate and present value calculations, ensuring appropriate selection based on project characteristics.

Tip 7: Seek Professional Advice: For complex or high-stakes projects, consider consulting a financial advisor or expert to guide the discount rate calculation process.

Tip 8: Practice and Proficiency: Enhance your proficiency through regular practice with various discount rate calculation scenarios to develop a strong understanding of the concepts and calculator functions.

In summary, adhering to these tips empowers you with the knowledge and skills to calculate accurate and reliable discount rates using a BA II Plus calculator, leading to more informed financial decision-making.

In the next section, we will delve into the limitations and pitfalls associated with discount rate calculations, providing guidance on how to mitigate potential errors and biases.

Conclusion

This comprehensive guide has illuminated the intricacies of calculating the discount rate on a BA II Plus calculator, equipping you with the knowledge and skills to make informed financial decisions. Key takeaways include the significance of considering project risk, inflation, and the impact of compounding frequency.

Remember, the accuracy and reliability of your discount rate calculations heavily influence the validity of your investment decisions. By adhering to the tips and best practices outlined in this article, you can mitigate potential errors and biases, leading to more confident and successful financial outcomes. Embrace the power of the BA II Plus calculator as a tool to navigate the complexities of time value of money and unlock the potential for sound financial planning.