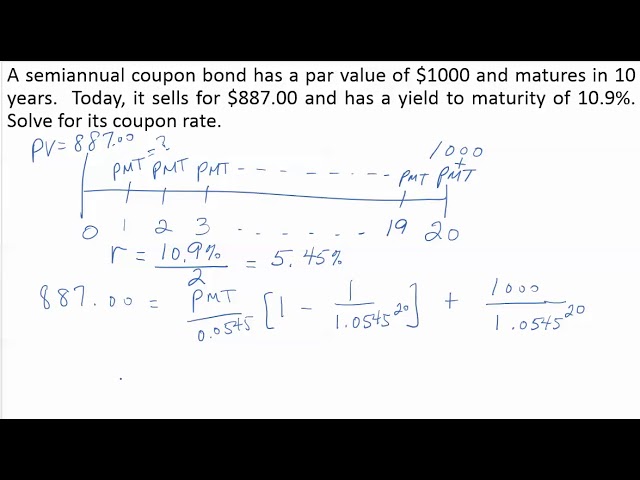

Calculating par coupon rate, a crucial element in fixed income securities, involves determining the interest rate payable on a bond relative to its face value. For instance, a bond with a $1,000 face value and a par coupon rate of 5% would pay $50 in interest each year.

Understanding par coupon rate is essential for investors seeking to assess bond values and compare yields. It enables informed decisions about portfolio allocations and helps mitigate financial risks. Historically, the development of standardized coupon rates has played a significant role in facilitating bond markets.

This article will delve into the intricacies of calculating par coupon rate, exploring its formula, influencing factors, and practical applications. Whether you’re a seasoned investor or just starting to navigate fixed income, this comprehensive guide will provide the insights you need to make sound financial decisions.

How to Calculate Par Coupon Rate

Understanding the essential aspects of calculating par coupon rate is crucial for informed decision-making in fixed income investments.

- Face Value

- Maturity Date

- Coupon Rate

- Par Value

- Bond Price

- Yield to Maturity

- Interest Payment

- Bond Rating

- Market Conditions

These aspects are interconnected and influence the overall calculation of par coupon rate. For instance, the face value and coupon rate determine the interest payment, while the bond price and yield to maturity reflect market demand and risk. By considering these factors, investors can assess the attractiveness and potential returns of a particular bond.

Face Value

Face value is the principal amount of a bond, representing the sum that the issuer owes to the bondholder at maturity. It serves as the basis for calculating the par coupon rate, which determines the interest payments the bond will make over its lifetime.

- Principal Amount: The face value is the amount of money that the borrower receives when the bond is issued and that the lender expects to receive back at maturity.

- Bond Certificate: The face value is typically printed on the bond certificate, along with other key information such as the coupon rate and maturity date.

- Par Value: The par value of a bond is equal to its face value. When a bond is trading at par, its market price is equal to its face value.

- Callable Bonds: Some bonds may have a callable feature, which gives the issuer the option to redeem the bonds before maturity. The call price is typically set at or above the face value.

Understanding the concept of face value is crucial for investors to accurately calculate the par coupon rate and assess the potential return on their bond investments.

Maturity Date

The maturity date is a critical component in calculating the par coupon rate as it determines the duration of the bond and the total amount of interest payments that will be made over its lifetime. A bond’s maturity date is the specific date on which the principal amount of the bond becomes due and payable to the bondholder. It is a crucial factor that influences the bond’s price, yield, and overall return.

The par coupon rate is calculated as a percentage of the bond’s face value and is paid semi-annually until the maturity date. The maturity date, therefore, directly impacts the total number of coupon payments that will be made during the bond’s life. For instance, a bond with a maturity date of 10 years and a par coupon rate of 5% will make 20 semi-annual coupon payments of $25 each.

Understanding the relationship between maturity date and par coupon rate is essential for investors to accurately assess the potential return and risk associated with a particular bond investment. By considering the maturity date, investors can make informed decisions about the duration of their investment and the frequency of interest payments they will receive. This understanding is particularly important in the context of interest rate fluctuations and changes in market conditions.

Coupon Rate

Coupon rate plays a pivotal role in calculating the par coupon rate of a bond, directly influencing the amount of interest payments an investor receives over the bond’s lifetime. It is expressed as an annual percentage of the bond’s face value and provides a baseline for assessing the bond’s yield and overall attractiveness to investors.

- Fixed vs. Variable: Coupon rates can be either fixed, remaining constant throughout the bond’s life, or variable, fluctuating based on an underlying benchmark or index.

- Semi-Annual Payments: Coupon payments are typically made semi-annually, providing investors with a regular stream of income. The par coupon rate is calculated based on these semi-annual payments.

- Market Conditions: Coupon rates are heavily influenced by market conditions, with higher rates offered during periods of economic uncertainty to attract investors.

- Credit Risk: The coupon rate also reflects the creditworthiness of the bond issuer, with higher rates indicating a higher perceived risk of default.

Understanding the various facets of coupon rate is crucial for investors to accurately calculate the par coupon rate and make informed decisions about their bond investments. By considering the type of coupon rate, payment schedule, market conditions, and credit risk, investors can assess the potential return and risk associated with a particular bond and tailor their investment strategies accordingly.

Par Value

Par value, representing the face value of a bond, stands as a crucial component in the calculation of par coupon rate. It serves as the foundation upon which the coupon payments, a defining characteristic of fixed income securities, are determined. The par value directly influences the interest payments an investor receives over the bond’s lifetime, impacting its overall yield and attractiveness.

To illustrate, consider a bond with a par value of $1,000 and a par coupon rate of 5%. The par coupon rate signifies that the bond will pay annual interest payments of $50, calculated as 5% of the $1,000 par value. These interest payments are typically made semi-annually, providing investors with a regular stream of income.

Understanding the relationship between par value and par coupon rate empowers investors to make informed decisions regarding bond investments. By considering the par value, investors can assess the potential return and risk associated with a particular bond and align their investment strategies accordingly. This understanding is particularly valuable in fixed income portfolios, where consistent income generation and capital preservation are key objectives.

Bond Price

Bond price plays a crucial role in calculating the par coupon rate, as it determines the present value of the bond’s future cash flows. Understanding the various facets of bond price is essential for investors to accurately assess the potential return and risk associated with a particular bond investment.

- Face Value: The face value, also known as the par value, represents the principal amount of the bond that the issuer owes to the bondholder at maturity. It serves as the basis for calculating both the par coupon rate and the bond’s price.

- Coupon Payments: Coupon payments are the periodic interest payments made to bondholders, typically semi-annually. The par coupon rate determines the dollar amount of each coupon payment.

- Maturity Date: The maturity date is the specific date on which the principal amount of the bond becomes due and payable to the bondholder. The time remaining until maturity is a key factor in determining the bond’s price.

- Market Interest Rates: Market interest rates, particularly prevailing yields on similar bonds, have a significant impact on bond prices. When market interest rates rise, bond prices tend to fall, and vice versa.

In summary, the bond price reflects the present value of the bond’s future cash flows, which include the par coupon rate, face value, maturity date, and prevailing market interest rates. By understanding these facets, investors can make informed decisions about their bond investments and assess the potential return and risk associated with different bonds.

Yield to Maturity

Yield to Maturity (YTM) holds a pivotal position in the realm of fixed income securities, providing valuable insights into the overall return an investor can expect from a bond investment. It serves as a crucial component in the calculation of the par coupon rate, offering a comprehensive measure of the bond’s attractiveness relative to prevailing market conditions.

- Current Market Price: YTM reflects the current market price of the bond, taking into account factors such as prevailing interest rates, creditworthiness of the issuer, and time to maturity.

- Future Cash Flows: YTM encapsulates the present value of all future cash flows associated with the bond, including both coupon payments and the final repayment of principal at maturity.

- Maturity Date: The maturity date of the bond is a key determinant of YTM, as it influences the duration and risk profile of the investment.

- Interest Rate Environment: YTM is highly sensitive to changes in the interest rate environment. As interest rates fluctuate, the market value of bonds and their corresponding YTMs adjust accordingly.

Understanding the intricate relationship between Yield to Maturity and the par coupon rate empowers investors to make informed decisions about their fixed income investments. By considering the various facets of YTM, investors can accurately assess the potential return and risk associated with different bonds and align their investment strategies accordingly.

Interest Payment

Interest payment plays a central role in calculating the par coupon rate, which is a critical metric used to determine the periodic interest payments made to bondholders. The par coupon rate is a fixed percentage of the bond’s face value, and it directly influences the amount of interest paid to investors over the life of the bond.

To illustrate the connection, let’s consider a bond with a face value of $1,000 and a par coupon rate of 5%. This means that the bondholder will receive annual interest payments of $50, calculated as 5% of the face value. The interest payment is a critical component of the par coupon rate, as it determines the regular income stream that investors can expect from the bond.

Understanding the relationship between interest payment and par coupon rate is essential for investors to make informed decisions about their fixed-income investments. By considering the par coupon rate, investors can assess the potential return and risk associated with different bonds and align their investment strategies accordingly. This understanding is particularly valuable in fixed-income portfolios, where consistent income generation and capital preservation are key objectives.

Bond Rating

Bond rating is a crucial aspect in calculating the par coupon rate, as it heavily influences the perceived risk and attractiveness of a bond to investors. Bond rating agencies, such as Moody’s and Standard & Poor’s, evaluate the creditworthiness of bond issuers and assign ratings that reflect the likelihood of timely interest payments and repayment of principal.

- Creditworthiness: Bond rating agencies assess the financial strength and stability of the bond issuer, considering factors such as revenue, debt levels, and management quality.

- Default Risk: The bond rating indicates the level of default risk associated with the bond, ranging from minimal risk (AAA) to high risk (D).

- Interest Rate Sensitivity: Bonds with lower ratings are more sensitive to interest rate changes, as investors demand higher returns to compensate for the increased risk of default.

- Investment Grade vs. Non-Investment Grade: Bonds rated BBB and above are considered investment grade, while those rated below are considered non-investment grade or “junk bonds.”

Understanding bond ratings is critical for investors to accurately calculate the par coupon rate and assess the potential return and risk of bond investments. Higher-rated bonds typically have lower par coupon rates, reflecting the lower perceived risk of default. Conversely, lower-rated bonds offer higher par coupon rates to compensate investors for the increased risk. By considering bond ratings in conjunction with other factors such as maturity date and yield to maturity, investors can make informed decisions about the suitability of different bonds for their investment portfolios.

Market Conditions

Market conditions play a significant role in the calculation of par coupon rates, influencing the overall yield and attractiveness of bonds to investors. These conditions encompass various economic and financial factors that affect the demand and supply dynamics of the bond market.

- Economic Growth:

Periods of strong economic growth often lead to higher interest rates, as businesses and consumers demand more capital for expansion. This can result in lower par coupon rates on new bond issues, as investors seek higher returns in other asset classes. - Inflation:

Inflation erodes the purchasing power of future cash flows, making investors less willing to accept lower par coupon rates. As a result, bonds issued during inflationary periods typically offer higher par coupon rates to compensate investors for the potential loss of value. - Interest Rate Expectations:

The market’s expectations about future interest rates can significantly impact par coupon rates. If investors anticipate rising interest rates, they may demand higher par coupon rates on new bond issues to lock in current yields before rates increase. - Supply and Demand:

The overall supply and demand for bonds in the market can also influence par coupon rates. When there is high demand for bonds, issuers may be able to offer lower par coupon rates, as investors are willing to accept lower yields in exchange for the safety and liquidity of bonds.

Understanding market conditions and their impact on par coupon rates is essential for investors to make informed decisions about their fixed income investments. By considering these factors, investors can assess the potential return and risk associated with different bonds and align their investment strategies accordingly.

Frequently Asked Questions

This section addresses common questions and concerns related to calculating par coupon rates, providing clarity and additional insights on the topic.

Question 1: What is the difference between par coupon rate and yield to maturity?

Answer: Par coupon rate is a fixed percentage of the bond’s face value that determines the periodic interest payments, while yield to maturity (YTM) is the annualized rate of return an investor can expect to receive if they hold the bond until maturity.

Question 2: How does the bond rating affect the par coupon rate?

Answer: Bonds with higher credit ratings typically have lower par coupon rates because they are considered less risky, while bonds with lower credit ratings offer higher par coupon rates to compensate investors for the increased risk of default.

Question 3: What is the relationship between the par coupon rate and the bond price?

Answer: The par coupon rate is inversely related to the bond price. When interest rates rise, bond prices fall, resulting in higher par coupon rates to attract investors. Conversely, when interest rates fall, bond prices rise, leading to lower par coupon rates.

Question 4: How can I calculate the par coupon rate for a bond?

Answer: To calculate the par coupon rate, divide the annual coupon payment by the face value of the bond and multiply by 100. For example, a bond with a $1,000 face value and an annual coupon payment of $50 has a par coupon rate of 5%.

Question 5: What factors influence the par coupon rate?

Answer: The par coupon rate is influenced by various factors such as the bond’s maturity date, credit rating, market interest rates, and supply and demand dynamics in the bond market.

Question 6: Why is it important to understand how to calculate par coupon rates?

Answer: Understanding how to calculate par coupon rates is essential for investors to assess the potential return and risk of fixed income investments. It enables informed decision-making and helps investors tailor their investment strategies accordingly.

These FAQs provide a concise overview of key considerations related to par coupon rates. To further delve into the nuances of bond valuation and investment strategies, the next section will explore advanced topics and provide additional insights for investors.

Tips for Calculating Par Coupon Rates

This section provides practical tips to assist you in accurately calculating par coupon rates, empowering you to make informed investment decisions.

Tip 1: Determine the Bond’s Face Value: Establish the principal amount of the bond, which serves as the basis for coupon payment calculations.

Tip 2: Identify the Maturity Date: Determine the specific date when the bond’s principal becomes due, influencing the duration of coupon payments.

Tip 3: Calculate the Annual Coupon Payment: Multiply the bond’s face value by the par coupon rate expressed as a decimal.

Tip 4: Consider Market Interest Rates: Assess prevailing interest rates to gauge the potential impact on bond prices and par coupon rates.

Tip 5: Utilize Online Calculators: Leverage readily available online tools to simplify the par coupon rate calculation process.

Tip 6: Seek Professional Advice: Consult with a financial advisor or bond specialist for personalized guidance and tailored recommendations.

Tip 7: Review Bond Prospectus: Refer to the bond prospectus for detailed information regarding coupon payment schedules and other relevant terms.

By following these tips, you can enhance the accuracy of your par coupon rate calculations and make more informed investment decisions. Understanding par coupon rates empowers you to assess the potential return and risk associated with fixed income investments, enabling you to optimize your portfolio performance.

In the concluding section, we will delve into advanced strategies and considerations for calculating par coupon rates, providing you with a comprehensive understanding of this critical aspect of bond valuation.

Conclusion

Our exploration of par coupon rate calculation has illuminated key concepts and their interconnectedness. Firstly, the par coupon rate directly influences the interest payments investors receive over the bond’s life, impacting its yield and attractiveness.

Furthermore, external factors such as market interest rates and economic conditions play a crucial role in determining par coupon rates, highlighting the dynamic nature of bond valuation. Understanding these factors enables investors to make informed decisions about their fixed income investments.

In conclusion, calculating par coupon rates accurately requires a holistic approach that considers various factors and their interrelationships. By mastering this aspect of bond valuation, investors can optimize their investment strategies, assess potential returns, and mitigate risks in the ever-evolving financial landscape.