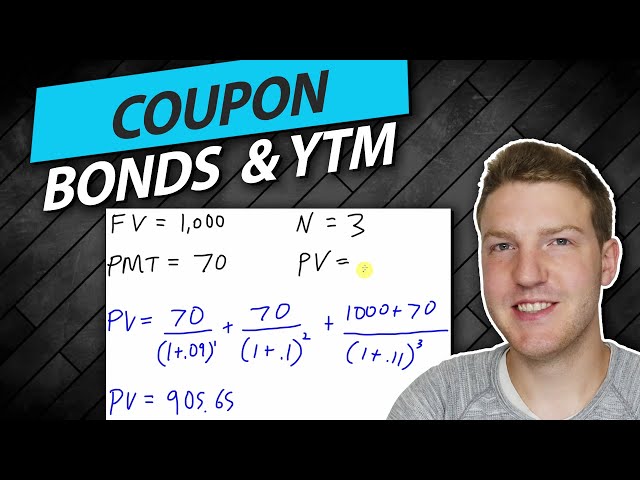

Yield to maturity (YTM) calculation on discount bonds is a crucial financial concept.

This calculation determines the annual rate of return an investor would earn if they held a bond until its maturity date.

Understanding YTM empowers investors to make informed decisions when investing in discount bonds.

how to calculate yield to maturity on discount bond

Understanding how to calculate yield to maturity (YTM) on discount bonds is crucial for investors seeking maximum returns on their bond investments.

- Principal Value

- Coupon Payments

- Maturity Date

- Present Value

- YTM Formula

- Discount Rate

- Bond Price

- Investment Horizon

- Interest Rate Fluctuations

These aspects collectively determine the YTM, providing insights into the bond’s potential return and risk profile. Understanding these aspects empowers investors to make informed decisions and optimize their investment strategies.

Principal Value

In the context of yield to maturity (YTM) calculation for discount bonds, the principal value plays a pivotal role. The principal value represents the face amount of the bond, which is the amount the issuer of the bond is obligated to repay to the bondholder at maturity. It acts as the foundation upon which the YTM is calculated, influencing its overall value.

The relationship between principal value and YTM is inverse. A higher principal value results in a lower YTM, and vice versa. This inverse relationship stems from the fact that a higher principal value implies a lower return on investment for the bondholder. Conversely, a lower principal value leads to a higher YTM, offering a potentially more attractive return.

Understanding the connection between principal value and YTM is crucial for investors seeking optimal returns. By carefully considering the principal value in conjunction with other factors that influence YTM, investors can make informed decisions about which discount bonds to invest in and align their investments with their financial goals.

Coupon Payments

Coupon payments are a crucial aspect of discount bonds and play a significant role in the calculation of yield to maturity (YTM). They represent periodic interest payments made to bondholders throughout the bond’s life, providing a steady stream of income.

- Fixed Amount: Coupon payments are typically fixed at a predetermined rate, providing bondholders with a predictable income stream.

- Payment Frequency: Coupon payments are usually made semi-annually or annually, with the frequency specified in the bond’s prospectus.

- Impact on Bond Price: Higher coupon payments generally lead to a higher bond price, as investors are willing to pay more for the regular income stream.

- YTM Calculation: Coupon payments are a key input in the YTM formula, as they represent the periodic cash flows received by bondholders.

Understanding the role of coupon payments is essential for investors seeking to accurately calculate YTM on discount bonds. By considering the fixed amount, payment frequency, impact on bond price, and relevance to YTM calculation, investors can gain a comprehensive view of how coupon payments influence the overall return on their bond investments.

Maturity Date

Within the context of yield to maturity (YTM) calculation for discount bonds, the maturity date holds critical importance. The maturity date represents the specific date on which the bond matures, marking the end of its life cycle. It directly influences the calculation of YTM, as it determines the duration over which interest accrues and the principal amount is repaid.

The relationship between maturity date and YTM is intrinsic. A shorter maturity date typically leads to a lower YTM, while a longer maturity date generally results in a higher YTM. This relationship arises because longer-term bonds are subject to greater interest rate risk and inflation risk, warranting a higher return to compensate investors for the associated uncertainty.

In practical terms, understanding the impact of maturity date on YTM empowers investors to make informed decisions about their bond investments. By carefully considering the maturity date in conjunction with other factors that influence YTM, investors can align their investments with their financial goals and risk tolerance. For instance, investors seeking a stable income stream may prefer bonds with shorter maturity dates and lower YTMs, while those willing to assume more risk may opt for bonds with longer maturity dates and potentially higher YTMs.

Present Value

Present value (PV) plays a critical role in the calculation of yield to maturity (YTM) on discount bonds, establishing a fundamental connection between the two concepts. PV represents the current value of a future cash flow, discounted back to the present using a specified discount rate. In the context of discount bonds, the future cash flows are the periodic coupon payments and the final principal repayment at maturity. These cash flows are discounted back to the present using the YTM as the discount rate.

The relationship between PV and YTM is reciprocal. A higher YTM leads to a lower PV, as the future cash flows are discounted at a higher rate. Conversely, a lower YTM results in a higher PV, as the future cash flows are discounted at a lower rate. This relationship is crucial for investors seeking to understand the potential return on their bond investments.

In practical terms, understanding the connection between PV and YTM empowers investors to make informed decisions about bond pricing and investment strategies. By considering the impact of YTM on PV, investors can determine the fair value of a discount bond and assess its potential return compared to other investment options. For instance, if an investor believes that the current YTM on a discount bond is too high, they may choose to purchase the bond, as they anticipate that the bond’s price will increase as the YTM falls.

YTM Formula

The YTM formula is a crucial component in calculating the yield to maturity (YTM) of discount bonds, providing a standardized approach to assess the potential return on investment.

- Bond Price: Represents the current market price of the bond, which is influenced by factors such as interest rates, credit risk, and supply and demand.

- Coupon Payments: Refers to the periodic interest payments made to bondholders throughout the life of the bond, typically semi-annually or annually.

- Maturity Date: Indicates the specific date on which the bond matures and the principal amount is repaid to bondholders.

- Discount Rate: Represents the annual rate of return that equates the present value of the bond’s future cash flows (coupon payments and principal repayment) to its current market price.

Understanding the components of the YTM formula empowers investors to accurately calculate the potential return on their discount bond investments. By considering the interrelationship between these factors, investors can make informed decisions about bond pricing, investment strategies, and risk tolerance.

Discount Rate

The discount rate is a crucial component in calculating the yield to maturity (YTM) of discount bonds. It represents the annual rate of return that equates the present value of the bond’s future cash flows (coupon payments and principal repayment) to its current market price. The discount rate is a critical factor that influences the YTM of a discount bond, with an inverse relationship between the two. A higher discount rate results in a lower YTM, and vice versa.

Real-life examples of the discount rate’s impact on YTM can be observed in the bond market. For instance, if the prevailing market interest rates rise, the discount rate used to calculate the YTM of a discount bond will also increase. Consequently, the YTM of the bond will decrease, making the bond less attractive to investors.

Understanding the connection between the discount rate and YTM is essential for investors seeking to make informed decisions about discount bond investments. By considering the impact of the discount rate on YTM, investors can assess the potential return on their investments and make strategic choices that align with their financial goals and risk tolerance.

Bond Price

In the realm of fixed-income investments, “bond price” and “how to calculate yield to maturity on discount bond” are inextricably intertwined. The bond price serves as a linchpin in the calculation of yield to maturity (YTM), which represents the annual rate of return an investor can expect to earn if they hold a bond until its maturity date.

The relationship between bond price and YTM is inverse. A higher bond price leads to a lower YTM, while a lower bond price results in a higher YTM. This inverse relationship stems from the fact that the YTM is calculated as the discount rate that equates the present value of the bond’s future cash flows (coupon payments and principal repayment) to its current market price. As the bond price increases, the present value of the future cash flows also increases, necessitating a lower discount rate (YTM) to equate the two.

Real-life examples abound in the bond market, illustrating the impact of bond price on YTM. For instance, if the market interest rates rise, the bond price will typically fall, as investors demand a higher return to compensate for the increased interest rate risk. Consequently, the YTM of the bond will increase, reflecting the lower bond price.

Understanding the connection between bond price and YTM is of paramount importance for investors seeking to make informed decisions about their bond investments. By considering the impact of bond price on YTM, investors can assess the potential return on their investments and make strategic choices that align with their financial goals and risk tolerance.

Investment Horizon

In the context of calculating yield to maturity (YTM) on discount bonds, investment horizon plays a crucial role in determining the potential return and risk profile of the investment. It represents the length of time for which an investor intends to hold the bond until its maturity date.

- Time Horizon: The specific period for which the investor plans to hold the bond, influencing the calculation of YTM and the overall investment strategy.

- Interest Rate Expectations: The investor’s expectations regarding future interest rate movements can impact their investment horizon and YTM calculations. For instance, if interest rates are anticipated to rise, investors may opt for shorter investment horizons to mitigate interest rate risk.

- Bond Maturity: The maturity date of the discount bond directly influences the investment horizon, as it determines the duration for which the investor will receive coupon payments and eventually the principal repayment.

- Investment Goals: The investor’s financial goals and risk tolerance can shape their investment horizon. For example, investors seeking capital preservation may prefer shorter investment horizons, while those seeking higher returns may opt for longer horizons.

Understanding the connection between investment horizon and YTM empowers investors to make informed decisions about their bond investments. By carefully considering their investment horizon in conjunction with other factors that influence YTM, investors can align their investimentos with their financial objectives.

Interest Rate Fluctuations

Interest rate fluctuations play a pivotal role in calculating the yield to maturity (YTM) of discount bonds, establishing a dynamic relationship between the two. Changes in interest rates directly affect the present value of the bond’s future cash flows, which in turn influences the YTM.

When interest rates rise, the present value of the bond’s future cash flows decreases, leading to a lower YTM. This occurs because investors demand a higher return to compensate for the increased opportunity cost of holding the bond. Conversely, when interest rates fall, the present value of the bond’s future cash flows increases, resulting in a higher YTM.

Real-life examples of interest rate fluctuations impacting YTM can be observed in the bond market. For instance, during periods of economic growth and rising inflation, central banks may increase interest rates to curb inflation. This leads to a decrease in bond prices and a corresponding increase in YTMs, as investors seek higher returns.

Understanding the connection between interest rate fluctuations and YTM is critical for investors seeking to make informed decisions about discount bond investments. By considering the impact of interest rate changes on YTM, investors can assess the potential risk and return of their investments and make strategic choices that align with their financial goals and risk tolerance.

Frequently Asked Questions

This section provides answers to common questions regarding the calculation of yield to maturity (YTM) on discount bonds.

Question 1: What factors influence the YTM of a discount bond?

The YTM of a discount bond is influenced by several factors, including the bond’s coupon rate, maturity date, present value, and current market price.

Question 2: How does the bond’s coupon rate affect its YTM?

A higher coupon rate generally leads to a higher YTM, as investors demand a higher return for bonds with higher coupon payments.

Question 3: What is the relationship between the bond’s maturity date and its YTM?

Longer maturity bonds typically have higher YTMs due to the increased risk and uncertainty associated with longer-term investments.

Question 4: How is the present value of a bond calculated?

The present value of a bond is calculated by discounting the bond’s future cash flows (coupon payments and principal repayment) back to the present using the YTM as the discount rate.

Question 5: What is the significance of the bond’s current market price in YTM calculation?

The bond’s current market price represents the present value of the bond’s future cash flows, and it is used to solve for the YTM using the YTM formula.

Question 6: How can investors use YTM to make informed investment decisions?

Understanding YTM allows investors to compare the potential returns of different discount bonds and make informed decisions about which bonds to invest in based on their risk tolerance and investment goals.

These FAQs provide a foundation for understanding the key factors that influence the YTM of discount bonds. In the next section, we will delve deeper into the practical aspects of YTM calculation.

Tips to Enhance Your Understanding of Yield to Maturity (YTM) on Discount Bonds

This section provides practical tips to help you grasp the nuances of YTM calculation and its implications for discount bond investments.

Tip 1: Understand Bond Basics: Familiarize yourself with bond terminology, including coupon payments, maturity dates, and face value, to lay a solid foundation for YTM calculation.

Tip 2: Grasp the Time Value of Money: Recognize the concept of discounting future cash flows back to their present value, a fundamental principle underlying YTM calculation.

Tip 3: Employ YTM Formula: Utilize the YTM formula, which incorporates bond price, coupon payments, and maturity date, to determine the annualized rate of return for discount bonds.

Tip 4: Consider Interest Rate Impact: Understand how changes in interest rates affect bond prices and, consequently, YTM, as interest rate fluctuations can influence the present value of future cash flows.

Tip 5: Analyze Bond Ratings: Incorporate bond ratings into your YTM calculations, as they provide insights into the creditworthiness of the bond issuer and can influence the perceived risk and expected return.

Tip 6: Evaluate Investment Horizon: Determine your investment horizon and align it with the bond’s maturity date, as this will impact the duration of your investment and the potential return you can expect.

Tip 7: Use YTM for Investment Decisions: Utilize YTM to compare different discount bond investment options, assess their potential returns, and make informed decisions based on your financial goals.

By incorporating these tips into your approach, you can enhance your understanding of YTM calculation, empowering you to make more informed and strategic discount bond investment decisions.

The following section will delve deeper into advanced YTM calculation techniques, providing you with additional tools to refine your investment analysis and maximize your returns.

Conclusion

This article has provided a comprehensive exploration of yield to maturity (YTM) calculation for discount bonds. We have examined the key factors that influence YTM, including bond price, coupon payments, maturity date, and interest rate fluctuations.

Understanding YTM is crucial for investors seeking to make informed decisions about their bond investments. By utilizing the YTM formula and considering the interconnections between these factors, investors can assess the potential return and risk of discount bonds and align their investments with their financial goals.