Yield-to-Maturity (YTM) is a crucial financial calculation that determines the return an investor can expect to earn on a fixed income security, such as a bond. It takes into account the security’s coupon rate and the present value of its future cash flows.

Understanding how to calculate YTM is essential for investors looking to maximize their returns. It allows them to compare different investment options and make informed decisions. Historically, YTM has been calculated using complex formulas and financial tables. However, with the advent of technology, there are now online calculators that make the process more accessible.

This article will provide a step-by-step guide on how to calculate YTM using the coupon rate, discussing its importance and exploring its historical development.

how to calculate ytm with coupon rate

Understanding the essential aspects of calculating yield-to-maturity (YTM) using the coupon rate is crucial for investors seeking to maximize their returns. These aspects encompass:

- Present value

- Future cash flows

- Maturity date

- Interest rate

- Bond price

- Yield

- Return

- Risk

These aspects are interconnected and play a vital role in determining the overall YTM calculation. Present value and future cash flows are discounted using the interest rate to determine the bond’s value, which is then used to calculate the yield. The yield, in turn, provides insights into the return and risk associated with the investment. Understanding the interplay of these aspects enables investors to make informed decisions and optimize their investment strategies.

Present value

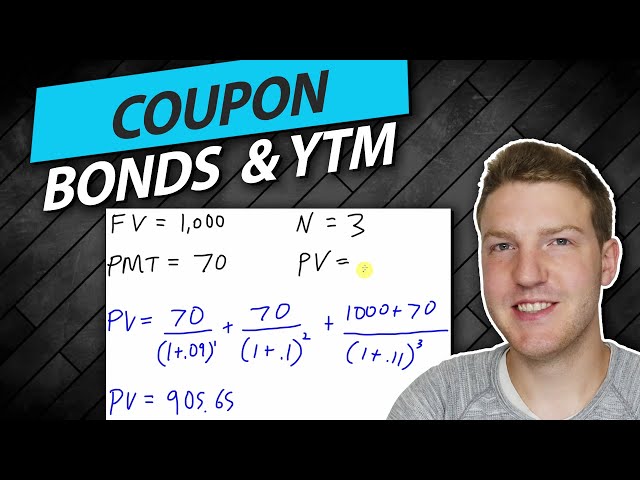

Present value plays a critical role in calculating yield-to-maturity (YTM), which is a crucial metric for evaluating fixed income investments. YTM represents the annualized rate of return an investor can expect to earn by holding a bond until its maturity date. To calculate YTM, one must discount the bond’s future cash flows, including coupon payments and the principal repayment at maturity, back to the present using the appropriate discount rate. This discount rate is typically determined by the prevailing market interest rates and the bond’s credit risk. The present value of these cash flows is then used to determine the bond’s current market price.

For example, consider a bond with a $1,000 face value, a 5% annual coupon rate, and a maturity date in 10 years. If the current market interest rate is 4%, the present value of the bond’s future cash flows would be approximately $900. This means that an investor could purchase this bond for $900 and expect to earn a 5% annual return if they hold it until maturity.

Understanding the relationship between present value and YTM is essential for investors seeking to make informed investment decisions. By understanding how changes in present value affect YTM, investors can better assess the potential risks and rewards of different fixed income investments.

Future cash flows

Future cash flows play a crucial role in the calculation of yield-to-maturity (YTM), as they represent the payments that an investor can expect to receive over the life of a bond. These cash flows include both the periodic coupon payments and the final repayment of the principal at maturity. The present value of these future cash flows is discounted back to the present using the YTM to determine the current market price of the bond.

- Coupon Payments: Coupon payments are the periodic interest payments made to bondholders. These payments are typically made semi-annually and are calculated as a percentage of the bond’s face value. Coupon payments are an important source of income for bondholders and are a key factor in determining the YTM of a bond.

- Maturity Date: The maturity date of a bond is the date on which the principal amount of the bond is repaid to the bondholder. The maturity date is a key factor in determining the YTM of a bond, as it affects the length of time over which the bondholder will receive coupon payments.

- Face Value: The face value of a bond is the amount of money that will be repaid to the bondholder at maturity. The face value is also known as the principal amount of the bond and is a key factor in determining the YTM of a bond, as it represents the amount of money that the bondholder will receive back at the end of the bond’s life.

Understanding the role of future cash flows in the calculation of YTM is essential for investors seeking to make informed investment decisions. By understanding how future cash flows affect YTM, investors can better assess the potential risks and rewards of different fixed income investments and optimize their investment strategies accordingly.

Maturity date

In the context of calculating yield-to-maturity (YTM) with coupon rate, the maturity date holds significant importance. It is the date on which the principal amount of the bond is repaid to the bondholder, marking the end of the bond’s life. Understanding the nuances of the maturity date is crucial for accurately calculating YTM.

- Length of Investment: The maturity date determines the length of time over which an investor will receive coupon payments and eventually receive the principal repayment. This affects the calculation of YTM, as the present value of future cash flows is discounted over the life of the bond.

- Interest Rate Risk: The maturity date influences the bond’s sensitivity to changes in interest rates. Bonds with longer maturities are generally more sensitive to interest rate fluctuations, which can impact YTM calculations.

- Callable Bonds: Some bonds may include a call feature, which allows the issuer to redeem the bond before its maturity date. This can affect YTM calculations, as the possibility of early repayment can alter the present value of future cash flows.

- Tax Implications: The maturity date can have tax implications for investors. Bonds held until maturity may qualify for favorable tax treatment, which can impact the overall return and YTM.

By considering the maturity date and its various facets, investors can gain a deeper understanding of how it affects the calculation of YTM. This knowledge empowers them to make informed decisions when evaluating and comparing different fixed income investments.

Interest rate

Interest rate plays a pivotal role in calculating Yield-to-Maturity (YTM) with coupon rate. It acts as the discount rate used to determine the present value of future cash flows associated with the bond. A higher interest rate leads to a lower present value and subsequently a lower YTM. Conversely, a lower interest rate results in a higher present value and a higher YTM. This inverse relationship is crucial in understanding the impact of interest rate on YTM calculations.

In real-world scenarios, interest rates fluctuate due to various economic factors, such as inflation, central bank policies, and market demand and supply. These fluctuations directly influence YTM calculations. For example, if interest rates rise, existing bonds with lower coupon rates become less attractive, leading to a decrease in their market prices and a rise in YTM. On the other hand, if interest rates fall, the demand for bonds with higher coupon rates increases, causing their market prices to rise and YTM to fall.

Understanding the connection between interest rate and YTM calculation is critical for investors. It enables them to assess the potential impact of interest rate changes on their bond investments and make informed decisions. By incorporating interest rate forecasts into YTM calculations, investors can better estimate the future returns on their fixed income investments and mitigate potential risks.

Bond price

In calculating Yield-to-Maturity (YTM) with coupon rate, bond price plays a pivotal role. It serves as the foundation upon which YTM is determined. YTM represents the internal rate of return (IRR) of an investment in a bond held until its maturity date, and it is heavily influenced by the bond’s price in the market.

There is an inverse relationship between bond price and YTM. When bond prices rise, YTM falls, and vice versa. This is because a higher bond price implies a lower yield, as investors are willing to pay more for the same stream of future cash flows. Conversely, a lower bond price suggests a higher yield, as investors demand a higher return to compensate for the lower purchase price.

Understanding this relationship is crucial for investors. By analyzing the bond price and its impact on YTM, investors can make informed decisions about when to buy or sell bonds. For example, if an investor expects interest rates to rise in the future, they may consider selling bonds with longer maturities, as these bonds are more sensitive to interest rate changes and could experience a decline in price. Alternatively, if an investor believes interest rates will fall, they may choose to buy bonds with higher coupon rates, as these bonds will benefit from a potential increase in their market value.

In summary, bond price is a critical component in calculating YTM with coupon rate, and understanding their relationship is essential for investors seeking to optimize their fixed income investments.

Yield

Understanding yield is essential when calculating Yield-to-Maturity (YTM) with coupon rate. Yield represents the return an investor can expect to earn from a bond investment, encompassing both the coupon payments and capital appreciation or depreciation over the bond’s life.

- Current Yield: Calculated as the annual coupon payment divided by the current market price of the bond, it provides a snapshot of the income an investor can expect in the current year.

- Yield-to-Maturity (YTM): As discussed earlier, YTM considers all future coupon payments and the repayment of principal at maturity, providing a more comprehensive measure of the return an investor can expect if the bond is held until its maturity date.

- Yield Spread: The difference between the YTM of a bond and a benchmark interest rate, such as the yield on government bonds, indicates the additional return an investor demands for taking on the credit risk associated with the bond.

- Yield Curve: A graphical representation of the relationship between yields and maturities across a range of bonds, the yield curve helps investors assess the market’s expectations for future interest rates.

In summary, yield is a multifaceted concept that encompasses various aspects such as current income, expected return, risk premium, and market expectations. Understanding these facets is crucial for investors seeking to make informed decisions when calculating YTM with coupon rate and evaluating fixed income investments.

Return

Understanding the concept of return is crucial in the context of calculating Yield-to-Maturity (YTM) with coupon rate. Return represents the financial gain or loss an investor realizes from an investment. In the case of bonds, return encompasses both the regular coupon payments received over the bond’s life and the capital appreciation or depreciation experienced upon its sale or maturity.

YTM, as discussed earlier, is a comprehensive measure of return that considers all future cash flows associated with a bond, including both coupon payments and the repayment of principal at maturity. It provides investors with a single metric representing the annualized rate of return they can expect if they hold the bond until its maturity date. In this sense, return is a critical component of YTM calculation, as it represents the ultimate financial outcome for the investor.

Real-world examples illustrate the relationship between return and YTM. Consider two bonds with identical face values and coupon rates but different maturities. The bond with a longer maturity will generally have a higher YTM, as investors demand a higher return for committing their funds for a more extended period. This is because longer-term bonds are more sensitive to interest rate fluctuations, which can impact their market value. As a result, investors require a higher yield to compensate for the potential risks associated with longer maturities.

Understanding the connection between return and YTM is essential for investors seeking to make informed decisions. By considering the potential return they can expect from a bond investment, investors can compare different options and select those that align with their investment goals and risk tolerance. Additionally, YTM calculations can help investors project their future cash flows and make informed decisions about their financial planning.

Risk

Risk is an inherent aspect of investing, and it plays a crucial role in the calculation of Yield-to-Maturity (YTM) with coupon rate. YTM represents the annualized rate of return an investor can expect to earn on a bond if held until maturity, but it does not account for the potential risks associated with the investment.

One of the primary risks associated with bonds is the risk of default. This refers to the possibility that the bond issuer may fail to make timely interest payments or repay the principal amount at maturity. Default risk is typically assessed based on the creditworthiness of the issuer, and it can have a significant impact on the YTM of a bond. Bonds issued by entities with lower credit ratings typically carry higher YTMs to compensate investors for the increased risk of default.

Another important risk to consider is interest rate risk. Interest rate risk refers to the potential impact of changes in interest rates on the value of a bond. When interest rates rise, the market value of existing bonds typically falls, as investors can now purchase new bonds with higher coupon rates. Conversely, when interest rates fall, the market value of existing bonds tends to rise. Interest rate risk is particularly relevant for bonds with longer maturities, as they are more sensitive to changes in interest rates.

Understanding the relationship between risk and YTM is critical for investors seeking to make informed investment decisions. By carefully considering the risks associated with a particular bond, investors can make more accurate assessments of the potential return and risk profile of the investment. This knowledge can help investors construct diversified portfolios that align with their individual risk tolerance and financial goals.

FAQs on Calculating Yield-to-Maturity (YTM) with Coupon Rate

This section addresses common questions and provides additional insights regarding the calculation of Yield-to-Maturity (YTM) using coupon rate.

Question 1: What is the significance of coupon rate in YTM calculation?

Answer: Coupon rate, representing the periodic interest payments on a bond, is a crucial factor in YTM calculation. It influences the present value of future cash flows, which is discounted to determine the YTM.

Question 2: How does maturity date affect YTM?

Answer: Maturity date determines the length of time until the bond matures and its principal is repaid. Longer maturities generally lead to higher YTMs due to increased interest rate risk.

Question 3: What is the relationship between interest rate and YTM?

Answer: Interest rate is the discount rate used in YTM calculation. Higher interest rates typically lead to lower YTMs, while lower interest rates result in higher YTMs.

Question 4: How can I calculate YTM using a calculator?

Answer: Financial calculators or online tools can simplify YTM calculations. They require inputs such as coupon rate, maturity date, bond price, and face value.

Question 5: What is the difference between current yield and YTM?

Answer: Current yield measures the annual return based on the current market price and coupon payments, while YTM considers all future cash flows until maturity.

Question 6: How does YTM help in investment decisions?

Answer: YTM provides a standardized metric to compare different bond investments. It enables investors to assess the potential return and risk associated with each bond based on its present value.

In summary, these FAQs highlight the importance of understanding the factors influencing YTM calculation and how YTM can assist investors in making informed fixed income investment decisions.

The following section of this article will delve deeper into the practical aspects of calculating YTM with coupon rate, providing step-by-step guidance and examples.

Tips for Calculating Yield-to-Maturity (YTM) with Coupon Rate

This section provides practical tips and step-by-step guidance to assist you in accurately calculating Yield-to-Maturity (YTM) with coupon rate. By following these tips, you can gain a deeper understanding of YTM and enhance your fixed income investment decision-making.

Tip 1: Gather the necessary information

To calculate YTM, you will need the bond’s coupon rate, maturity date, current market price, and face value.

Tip 2: Calculate the present value of future cash flows

Determine the present value of each future coupon payment and the repayment of the principal at maturity using the appropriate discount rate.

Tip 3: Use a financial calculator or online tool

Financial calculators or online tools can simplify YTM calculations by automating the process.

Tip 4: Consider the bond’s creditworthiness

The creditworthiness of the bond issuer can impact the YTM, as it influences the risk of default.

Tip 5: Analyze the current interest rate environment

Interest rates play a crucial role in YTM calculation. Understand the current interest rate environment and its potential impact on bond prices.

Tip 6: Compare YTMs of different bonds

Compare the YTMs of different bonds to assess their relative attractiveness considering risk and return.

Tip 7: Monitor YTM over time

YTM can fluctuate due to changes in interest rates and other factors. Monitor YTM over time to make informed decisions about your bond investments.

Tip 8: Seek professional advice if needed

If you are unsure about calculating YTM or have complex investment scenarios, consider seeking professional financial advice.

In summary, understanding and accurately calculating YTM with coupon rate is essential for informed fixed income investing. By following these tips, you can enhance your knowledge and make data-driven decisions to achieve your financial goals.

The next section of this article will explore advanced concepts related to YTM, providing insights into more complex scenarios and strategies.

Conclusion

In summary, calculating Yield-to-Maturity (YTM) with coupon rate is a fundamental aspect of fixed income investing. This article has provided a comprehensive exploration of the concept, emphasizing its significance, the factors that influence it, and practical tips for accurate calculation. It highlighted the interconnectedness of coupon rate, maturity date, bond price, and interest rate in determining YTM, enabling investors to make informed decisions.

Understanding YTM empowers investors to compare different bond investments, assess potential returns, and manage risk. By incorporating YTM calculations into their investment strategies, they can optimize their portfolios and achieve their financial goals. The insights gained from this article can serve as a valuable guide for investors seeking to navigate the complexities of fixed income markets.