Zero coupon bonds are debt instruments that pay no periodic interest payments and are sold at a substantial discount from their face value. An investor must calculate the yield on a zero-coupon bond by considering the difference between the offering price and its maturity value.

Zero-coupon bonds are popular among investors who seek steady returns and have low liquidity requirements. Their value has grown throughout time, especially after their introduction to the United States in the 1980s.

This article will provide a comprehensive guide to calculating the yield on zero-coupon bonds. We will cover various methods, including the present value approach.

Zero Coupon How To Calculate

When calculating zero coupon bonds, it is essential to consider factors such as present value, yield-to-maturity, and duration. These aspects are crucial for understanding the bond’s value and return.

- Present Value

- Yield-to-Maturity

- Duration

- Offering Price

- Maturity Value

- Time to Maturity

- Compounding Frequency

- Tax Implications

- Credit Risk

- Liquidity

By considering these aspects, you can determine the bond’s suitability based on your investment goals and risk tolerance. Understanding the relationship between these factors helps you make informed decisions when investing in zero-coupon bonds.

Present Value

Present Value plays a fundamental role in calculating the yield of zero-coupon bonds. It reflects the current worth of future cash flows, discounted at a specific rate. Zero-coupon bonds make a single payment at maturity, and their price is determined by discounting the maturity value back to the present using the yield-to-maturity as the discount rate.

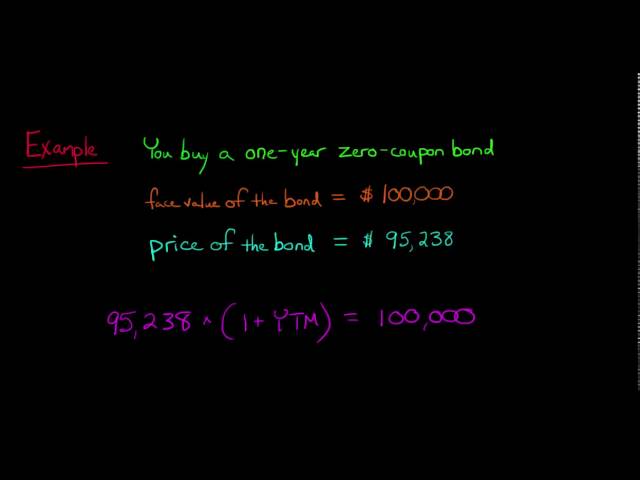

For instance, if a zero-coupon bond has a maturity value of $1,000, a time to maturity of 5 years, and a yield-to-maturity of 5%, the present value can be calculated as $1,000 / (1 + 0.05)^5 = $783.53. This present value represents the price an investor would pay for the bond today.

Understanding the relationship between Present Value and zero-coupon bond calculations is critical for investors as it enables them to determine the bond’s yield and make informed investment decisions. This concept finds practical applications in various financial scenarios, including bond pricing, portfolio management, and financial planning.

Yield-to-Maturity

Yield-to-Maturity (YTM) is a critical concept in calculating zero-coupon bond yields. It represents the annualized rate of return an investor expects to receive if they hold the bond until maturity.

- Bond Price: YTM influences the bond’s present value or purchase price. Higher YTM leads to a lower present value, making the bond more attractive for investors seeking higher returns.

- Maturity Date: The time remaining until the bond’s maturity significantly impacts YTM. Longer maturities generally result in higher YTM due to increased interest rate risk.

- Default Risk: Bonds issued by companies or governments with higher perceived credit risk typically carry higher YTM, reflecting the additional compensation demanded by investors for taking on default risk.

- Taxation: The tax treatment of bond returns can affect YTM calculations. Tax-free bonds, for example, may offer lower YTM than taxable bonds due to their reduced after-tax returns.

Understanding the relationship between Yield-to-Maturity and various factors is crucial for investors to make informed investment decisions. YTM allows them to compare different zero-coupon bonds and assess their potential returns and risks.

Duration

Duration is a crucial aspect of calculating zero-coupon bond yields, measuring the sensitivity of a bond’s price to changes in interest rates. Understanding its components allows investors to make informed decisions regarding bond investments.

- Macaulay Duration: Represents the weighted average time until the bond’s cash flows are received, considering both interest payments and the principal repayment. It is a measure of interest rate risk, with higher duration bonds experiencing greater price fluctuations in response to interest rate changes.

- Modified Duration: Similar to Macaulay Duration but measures the proportionate change in bond price for a given change in yield-to-maturity. It provides a more accurate estimate of bond price sensitivity, particularly for bonds with non-uniform cash flows.

- Effective Duration: Considers the reinvestment of coupon payments and measures the price impact of a change in yield to maturity on the present value of both future coupons and the principal payment. It is particularly relevant for long-term bonds and bonds with high coupon rates.

- Key Rate Duration: Measures the price sensitivity of a bond to changes in interest rates within a specific range, typically around the current yield-to-maturity. It helps investors assess the bond’s price behavior under different interest rate scenarios.

Understanding the various facets of Duration enables investors to gauge the potential price fluctuations of zero-coupon bonds in different interest rate environments. This information is essential for managing interest rate risk and making informed investment decisions.

Offering Price

When calculating zero coupon bonds, the Offering Price plays a crucial role. It signifies the price at which the bond is initially sold to investors and directly influences the bond’s yield. Understanding its components and implications is essential for accurate yield calculations.

- Face Value: The nominal or maturity value of the bond, which is repaid to the holder at maturity. The Offering Price is typically a discount from the Face Value.

- Market Conditions: Supply and demand dynamics in the bond market can impact the Offering Price. Higher demand for a bond can lead to a premium Offering Price, while lower demand may result in a discount.

- Creditworthiness: The financial health and credit rating of the bond issuer influence the Offering Price. Bonds issued by entities with higher credit ratings generally command a higher Offering Price.

- Time to Maturity: The length of time until the bond matures also affects the Offering Price. Bonds with longer maturities tend to have lower Offering Prices due to the increased interest rate risk associated with longer durations.

By considering these facets of the Offering Price, investors can gain a deeper understanding of zero coupon bond pricing and make informed decisions when investing in these instruments. The Offering Price not only determines the initial yield of the bond but also serves as a basis for calculating future cash flows and returns throughout the bond’s life.

Maturity Value

When calculating zero-coupon bonds, Maturity Value plays a crucial role as it represents the final payment received by the bondholder at the end of the bond’s term. Understanding the intricacies of Maturity Value is essential for accurate yield calculations and informed investment decisions.

Maturity Value directly influences the bond’s price and yield. Bonds with higher Maturity Values tend to have higher Offering Prices and lower yields since the investor receives a larger lump sum at maturity. Conversely, bonds with lower Maturity Values have lower Offering Prices and higher yields.

For example, consider two zero-coupon bonds with the same time to maturity but different Maturity Values. The bond with a Maturity Value of $1,000 will have a higher Offering Price and a lower yield compared to the bond with a Maturity Value of $500. This is because the investor is willing to pay a premium for the higher Maturity Value, resulting in a lower yield.

Understanding the relationship between Maturity Value and zero-coupon bond calculations is crucial for investors to assess the trade-off between bond price and yield. This knowledge empowers investors to make informed decisions when selecting zero-coupon bonds that align with their risk tolerance and return expectations.

Time to Maturity

In the realm of zero-coupon bond calculations, Time to Maturity holds immense significance. It represents the duration between the bond’s issuance and maturity dates, directly influencing the bond’s yield and price. A thorough understanding of this relationship is crucial for accurate yield calculations and informed investment decisions.

Time to Maturity exerts a profound influence on a zero-coupon bond’s yield. Generally, bonds with longer maturities have higher yields compared to those with shorter maturities. This is primarily due to the increased interest rate risk associated with longer-term bonds. Investors demand a higher return for committing their funds for an extended period, leading to higher yields.

For instance, consider two zero-coupon bonds issued by the same company, but with different Time to Maturity. The bond with a 10-year maturity would typically have a higher yield than the one with a 5-year maturity. The longer maturity exposes the investor to greater uncertainty in future interest rates, warranting a higher yield as compensation for the additional risk.

Understanding the connection between Time to Maturity and zero-coupon bond calculations is not only critical for yield determination but also for strategic investment decisions. Investors can tailor their bond portfolios based on their risk tolerance and investment horizon. By incorporating Time to Maturity into their analysis, they can mitigate interest rate risk and optimize their returns.

Compounding Frequency

In the context of zero-coupon bond calculations, Compounding Frequency plays a crucial role in determining the bond’s yield and present value. Compounding refers to the process of adding interest to the principal, which then earns interest in subsequent periods. The frequency of compounding directly affects the effective yield and return on the bond.

Higher Compounding Frequency leads to a higher yield and present value for the zero-coupon bond. This is because more frequent compounding results in a greater number of compounding periods, allowing the interest to accumulate at a faster rate. Conversely, lower Compounding Frequency results in a lower yield and present value.

For instance, consider two zero-coupon bonds with the same face value, maturity date, and yield-to-maturity. However, one bond compounds annually, while the other compounds semi-annually. The bond with semi-annual compounding will have a higher yield and present value due to the more frequent compounding periods.

Understanding the relationship between Compounding Frequency and zero-coupon bond calculations is essential for investors to accurately determine the bond’s yield and make informed investment decisions. By considering the impact of Compounding Frequency, investors can optimize their returns and tailor their bond portfolios to their financial goals.

Tax Implications

When evaluating “zero coupon how to calculate,” “Tax Implications” play a pivotal role in determining the effective yield and return on investment. Understanding “Tax Implications” and its components is crucial for investors to make informed investment decisions.

- Tax-Deferred Growth: Zero-coupon bonds offer tax-deferred growth, meaning no taxes are due on the accumulated interest until the bond matures or is sold.

- Taxation at Maturity: Upon maturity or sale, “Tax Implications” arise as the accumulated interest is taxed as ordinary income. This can significantly impact the overall return.

- State and Local Taxes: “Tax Implications” can vary depending on state and local tax laws. Some states may exempt zero-coupon bonds from local income taxes, while others may tax them at a reduced rate.

- Alternative Minimum Tax (AMT): Zero-coupon bonds can be subject to AMT, which imposes an additional tax on certain types of income, including the accumulated interest on zero-coupon bonds.

Investors should carefully consider “Tax Implications” when incorporating zero-coupon bonds into their portfolios. Understanding the potential tax consequences and consulting with a tax professional can help investors optimize their returns and minimize tax liability.

Credit Risk

When delving into “zero coupon how to calculate,” “Credit Risk” emerges as a significant factor influencing the evaluation and pricing of these bonds. “Credit Risk” refers to the possibility that the issuer of a bond may default on its obligation to make interest or principal payments, leading to a loss of investment for the bondholder.

In “zero coupon how to calculate,” “Credit Risk” plays a critical role because these bonds do not pay periodic interest payments. Instead, all interest is accumulated and paid at maturity. This means that investors in zero-coupon bonds are exposed to the full extent of “Credit Risk” for the entire term of the bond.

A real-life example of “Credit Risk” in “zero coupon how to calculate” can be seen in the case of the General Motors bankruptcy in 2009. GM issued zero-coupon bonds prior to its bankruptcy, and when the company filed for bankruptcy, the bondholders faced a significant loss as the company could not fulfill its obligation to pay the accumulated interest and principal.

Understanding the connection between “Credit Risk” and “zero coupon how to calculate” is crucial for investors. By assessing the “Credit Risk” associated with a zero-coupon bond, investors can make informed decisions about the potential risks and returns of the investment. This understanding enables investors to diversify their portfolios, mitigate risk, and optimize their overall investment strategy.

Liquidity

Liquidity, as it pertains to zero coupon how to calculate, is a crucial aspect that influences the ease with which these bonds can be bought or sold in the market. Understanding liquidity is essential for investors to gauge the potential for timely and efficient execution of trades, as well as its impact on overall investment strategies.

- Market Depth: Refers to the volume of outstanding zero-coupon bonds available for trading, which affects the ease of executing large orders without significantly impacting the market price.

- Bid-Ask Spread: Represents the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept, indicating the transaction costs associated with trading zero-coupon bonds.

- Trading Frequency: Measures the regularity with which zero-coupon bonds are traded, providing insights into the active participation of market participants and the potential for immediate execution of trades.

- Price Volatility: Assesses the extent to which zero-coupon bond prices fluctuate, affecting the potential for short-term gains or losses and the suitability for risk-averse investors.

Understanding these liquidity aspects enables investors to make informed decisions when investing in zero-coupon bonds. By considering factors such as market depth, bid-ask spread, trading frequency, and price volatility, investors can align their investment strategies with their risk tolerance, time horizon, and liquidity requirements.

Frequently Asked Questions on “Zero Coupon How to Calculate”

This section addresses common questions and clarifications regarding “zero coupon how to calculate.”

Question 1: What is the key difference between a zero-coupon bond and a regular coupon bond?

Zero-coupon bonds do not pay periodic interest payments like regular coupon bonds. Instead, they are sold at a deep discount and redeemed at maturity for their face value, providing a single lump sum return.

Question 2: How do I calculate the yield-to-maturity of a zero-coupon bond?

The yield-to-maturity is the annualized rate of return an investor can expect to receive if they hold the bond until maturity. It can be calculated using the formula: Yield-to-Maturity = (Face Value / Present Value)^(1 / Number of Years to Maturity) – 1

Question 3: What factors influence the price of a zero-coupon bond?

The price of a zero-coupon bond is affected by factors such as its face value, time to maturity, prevailing interest rates, and the creditworthiness of the issuer.

Question 4: Are zero-coupon bonds considered risky investments?

Like any fixed-income investment, zero-coupon bonds carry some level of risk. However, they are generally considered less risky than regular coupon bonds due to their lack of periodic interest payments.

Question 5: How are zero-coupon bonds taxed?

Zero-coupon bonds are subject to taxation when they mature or are sold. The accumulated interest is taxed as ordinary income.

Question 6: What is the difference between a stripped zero-coupon bond and a zero-coupon bond?

A stripped zero-coupon bond is created when the coupon payments are separated from a regular coupon bond and sold separately. Zero-coupon bonds, on the other hand, are issued without any coupon payments.

These FAQs provide a solid foundation for understanding the key aspects of “zero coupon how to calculate.” For further insights into advanced strategies and considerations, continue to the next section.

Transition to the next section: “Advanced Considerations in Zero Coupon Bond Calculations”

Zero Coupon Bond Calculation Tips

This section provides practical tips to enhance your understanding and accuracy when calculating zero-coupon bond yields and returns.

Tip 1: Use a financial calculator or spreadsheet: Specialized tools can simplify complex calculations and minimize errors.

Tip 2: Pay attention to compounding frequency: Accrued interest compounds over time, affecting the final yield.

Tip 3: Consider tax implications: Zero-coupon bonds have unique tax treatments that can impact your returns.

Tip 4: Assess credit risk: The issuer’s creditworthiness influences the bond’s yield and potential for default.

Tip 5: Factor in liquidity: Understand the ease of buying or selling the bond to meet your financial needs.

Tip 6: Compare different bonds: Evaluate multiple zero-coupon bonds to find the best fit for your investment goals.

Tip 7: Consult with a financial advisor: Seek professional guidance to optimize your zero-coupon bond investments.

Summary: By following these tips, you can enhance your ability to calculate zero-coupon bond yields and make informed investment decisions. Understanding these nuances can help you navigate the fixed-income market effectively.

Transition to Conclusion: These tips provide a solid foundation for understanding zero-coupon bond calculations. In the final section, we will delve into advanced techniques and strategies to further maximize your returns and mitigate risks.

Conclusion

In this article, we have explored the intricacies of “zero coupon how to calculate.” We have covered essential concepts such as present value, yield-to-maturity, duration, and tax implications, highlighting their interconnectedness in determining the value and returns of zero-coupon bonds.

Key takeaways include: understanding the time value of money is crucial for accurate yield calculations; assessing credit risk is essential to gauge the potential for default; and considering liquidity ensures that the bonds can be bought or sold as needed. By mastering these concepts, investors can make informed decisions when investing in zero-coupon bonds.